In partnership with

Gold hitting record highs

The price of gold keeps heating up. If the record-breaking year of 2024 wasn't enough, gold hit a major historic 2025 milestone by crossing the $3,000/ounce threshold!

Here are 3 Key Reasons:

Looming economic & political uncertainty

Increasing central bank demand

Rising National Debt - over $36 Trillion

So, could gold surge even higher?

According to a recent statement from Jeffrey Gundlach, famed American business man and investor… “Gold continues its bull market that we’ve been talking about for a couple of years, ever since it was down to $1,800.” He expects gold to reach $4,000/oz.

Is it time you learn more about precious metals?

Get all the answers in your free 2025 Gold & Silver Kit. Plus, if you request your free kit today, you could qualify for up to 10% Instant Match in Bonus Silver*.

*Offer valid on qualified orders of Goldco premium products only. Receive up to 10% in free silver based on purchase amount; cannot be combined with other offers. Additional terms apply—see your customer agreement or contact your representative for details.

Elaborated with Python

In today’s dynamic financial markets, sophisticated portfolio management requires more than traditional buy-and-hold strategies. This article introduces a Python implementation that combines hierarchical risk clustering with an adaptive long/short strategy, specifically designed for managing a portfolio of high-growth tech stocks, known as the “Magnificent Seven” (Apple, Microsoft, Google, Amazon, NVIDIA, Meta, and Tesla).

The Core Concepts

Before diving into the code, let’s understand the key concepts this implementation brings together:

Hierarchical Risk Clustering (HRC): This technique groups assets based on their correlation patterns, helping us diversify risk more effectively than traditional methods.

Risk-Adaptive Long/Short Strategy: Instead of always being long, our implementation switches between long positions in tech stocks and short positions in the S&P 500 (SPY) based on risk signals.

Multiple Risk Metrics: We combine drawdown limits, Value at Risk (VaR), and volatility measures to create a comprehensive risk management framework.

Let’s break down the implementation step by step.

Class Structure and Initialization

class HRCLongShortManager:

def __init__(self, start_date, n_clusters=3, confidence_level=0.99,

window=252, max_drawdown=-15):Our class initializes with several key parameters:

start_date: Beginning of our historical data periodn_clusters: Number of asset groups for risk clustering (default: 3)confidence_level: Confidence level for VaR calculations (default: 99%)window: Rolling window for volatility calculations (default: 252 trading days)max_drawdown: Maximum allowed drawdown (default: -15%)

Smarter Investing Starts with Smarter News

The Daily Upside helps 1M+ investors cut through the noise with expert insights. Get clear, concise, actually useful financial news. Smarter investing starts in your inbox—subscribe free.

Data Collection and Preparation

The download_data method handles data acquisition and initial processing:

def download_data(self):

symbols = self.magnificent_seven + ['SPY']

df_list = []

for symbol in symbols:

try:

data = yf.download(symbol, self.start_date)

df = data['Adj Close']

df_list.append(df)

except Exception as e:

print(f"Error downloading {symbol}: {e}")

continueThis method:

Downloads historical data for our tech stocks and SPY

Uses adjusted closing prices to account for corporate actions

Calculates returns and adds temporal information

Separates SPY returns for our long/short strategy

Hierarchical Risk Clustering

The clustering process is implemented in calculate_clusters:

def calculate_clusters(self):

corr_matrix = self.returns[self.magnificent_seven].corr()

dist_matrix = np.sqrt(2 * (1 - corr_matrix))

linkage_matrix = linkage(squareform(dist_matrix), method='ward')This method:

Calculates correlation matrix between assets

Converts correlations to distances (higher correlation = shorter distance)

Applies hierarchical clustering using Ward’s method

Groups similar assets together based on their risk characteristics

Portfolio Weight Calculation

The calculate_weights method implements our weighting strategy:

def calculate_weights(self):

variances = self.returns[self.magnificent_seven].var()

inv_variances = 1 / variances

self.weights = pd.Series(0, index=self.magnificent_seven)Key features:

Uses inverse variance weighting within clusters

Ensures equal risk contribution between clusters

Automatically adjusts weights based on asset volatility

Risk Metrics and Trading Signals

Our risk management system, implemented in calculate_portfolio_metrics, combines multiple risk measures:

def calculate_portfolio_metrics(self):

# Portfolio value and drawdown

self.portfolio_value = (1 + self.portfolio_returns).cumprod() * 100

self.drawdown = ((self.portfolio_value - self.rolling_max) / self.rolling_max) * 100

# Volatility and VaR calculations

self.daily_volatility = self.portfolio_returns.rolling(window=self.window).std()

z_score = norm.ppf(1 - self.confidence_level)

self.daily_var = self.daily_volatility * z_scoreThe system monitors:

Portfolio drawdown against maximum limits

Daily and weekly Value at Risk violations

Volatility trends at different time scales

Long/Short Strategy Implementation

The strategy switches between positions based on risk signals:

def backtest_portfolio(self):

backtest = pd.DataFrame(index=self.portfolio_returns.index)

backtest['Long_Position'] = (~backtest['Risk_Signal']).astype(int)

backtest['Short_Position'] = backtest['Risk_Signal'].astype(int) * -1When risk signals are triggered:

Exits long positions in tech stocks

Takes short positions in SPY

Maintains these positions until risk metrics improve

Performance Visualization and Analysis

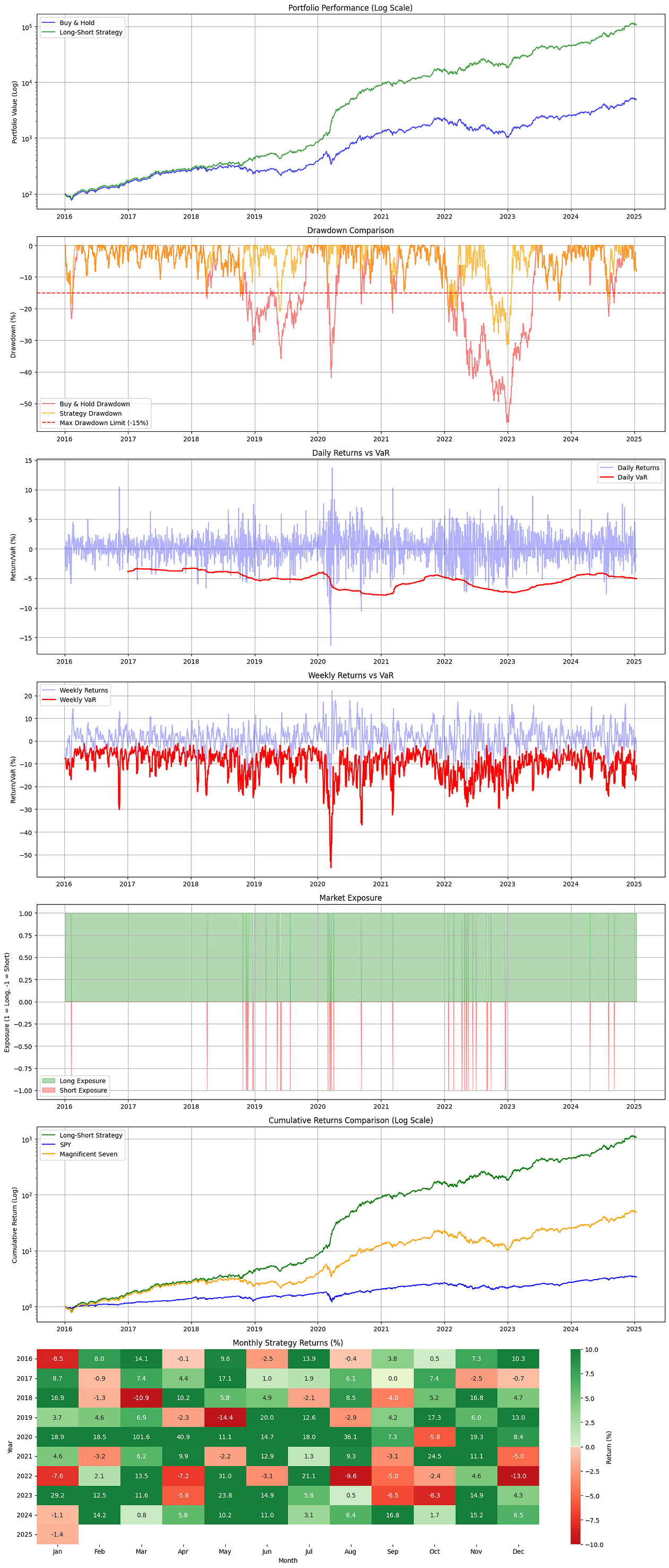

The code includes comprehensive visualization capabilities:

def plot_portfolio_analysis(self, backtest):

fig, axes = plt.subplots(7, 1, figsize=(15, 35))

# Performance plot

axes[0].semilogy(backtest.index, backtest['Strategy_Equity'],

label='Long-Short Strategy', color='green', alpha=0.7)Key visualizations include:

Portfolio performance on a log scale

Drawdown comparison with benchmark

VaR violations and risk metrics

Market exposure over time

Monthly returns heatmap with custom color scaling

Performance Statistics

The implementation calculates comprehensive performance metrics:

def _calculate_performance_stats(self, backtest, years, trading_days, initial_capital):

stats = {

'strategy': {

'annual_return': ((1 + strategy_total_return/100) ** (1/years) - 1) * 100,

'volatility': backtest['Strategy_Returns'].std() * np.sqrt(trading_days) * 100,

'sharpe': stats['strategy']['annual_return'] / stats['strategy']['volatility'],

'calmar': abs(stats['strategy']['annual_return'] / stats['strategy']['max_drawdown'])

}

}These statistics include:

Total and annualized returns

Risk-adjusted metrics (Sharpe and Calmar ratios)

Exposure metrics and trading frequency

Comparison with buy-and-hold strategy

Practical Implementation

To use this portfolio manager:

if __name__ == "__main__":

portfolio_manager = HRCLongShortManager('2016-01-01')

returns = portfolio_manager.download_data()

clusters = portfolio_manager.calculate_clusters()

weights = portfolio_manager.calculate_weights()

risk_signals = portfolio_manager.calculate_portfolio_metrics()

backtest_results = portfolio_manager.backtest_portfolio()Conclusion

This implementation offers a sophisticated approach to portfolio management by combining:

Smart risk clustering for diversification

Adaptive long/short positioning

Comprehensive risk management

Detailed performance analysis and visualization

The code is designed to be practical and suitable for both learning and real-world applications. While focused on the Magnificent Seven tech stocks, the approach can be adapted to other assets and markets.

The results are good enough, in theory. Also, did not used transactional costs.

=== Backtest Results (2016-2024) ===

Buy & Hold Statistics (Magnificent Seven):

Total Return: 4,748.37%

Annualized Return: 53.83%

Annualized Volatility: 36.57%

Sharpe Ratio: 1.47

Maximum Drawdown: -56.07%

Calmar Ratio: 0.96

Long-Short Strategy Statistics:

Total Return: 105,691.08%

Annualized Return: 116.57%

Annualized Volatility: 34.86%

Sharpe Ratio: 3.34

Maximum Drawdown: -31.50%

Calmar Ratio: 3.70

Long Exposure: 97.9%

Short Exposure: 2.1%

Number of Trades: 34