In partnership with

Join 400,000+ executives and professionals who trust The AI Report for daily, practical AI updates.

Built for business—not engineers—this newsletter delivers expert prompts, real-world use cases, and decision-ready insights.

No hype. No jargon. Just results.

🚀 Your Investing Journey Just Got Better: Premium Subscriptions Are Here! 🚀

It’s been 4 months since we launched our premium subscription plans at GuruFinance Insights, and the results have been phenomenal! Now, we’re making it even better for you to take your investing game to the next level. Whether you’re just starting out or you’re a seasoned trader, our updated plans are designed to give you the tools, insights, and support you need to succeed.

Here’s what you’ll get as a premium member:

Exclusive Trading Strategies: Unlock proven methods to maximize your returns.

In-Depth Research Analysis: Stay ahead with insights from the latest market trends.

Ad-Free Experience: Focus on what matters most—your investments.

Monthly AMA Sessions: Get your questions answered by top industry experts.

Coding Tutorials: Learn how to automate your trading strategies like a pro.

Masterclasses & One-on-One Consultations: Elevate your skills with personalized guidance.

Our three tailored plans—Starter Investor, Pro Trader, and Elite Investor—are designed to fit your unique needs and goals. Whether you’re looking for foundational tools or advanced strategies, we’ve got you covered.

Don’t wait any longer to transform your investment strategy. The last 4 months have shown just how powerful these tools can be—now it’s your turn to experience the difference.

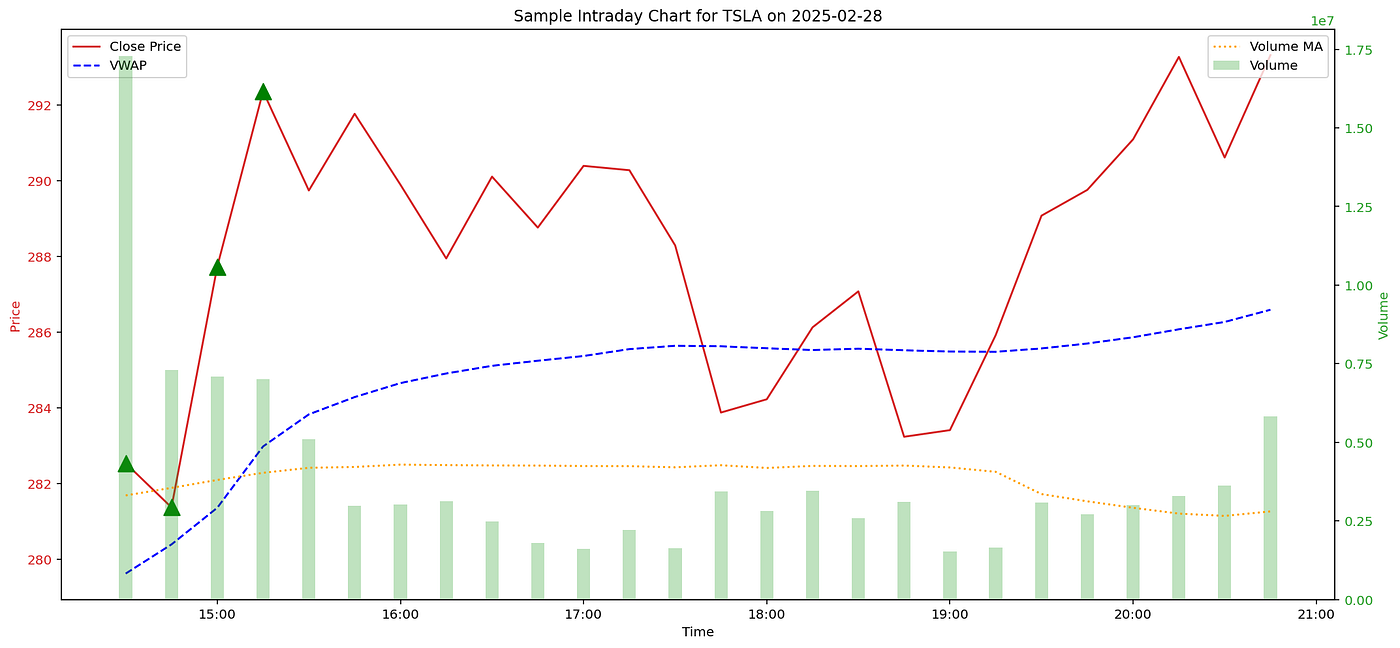

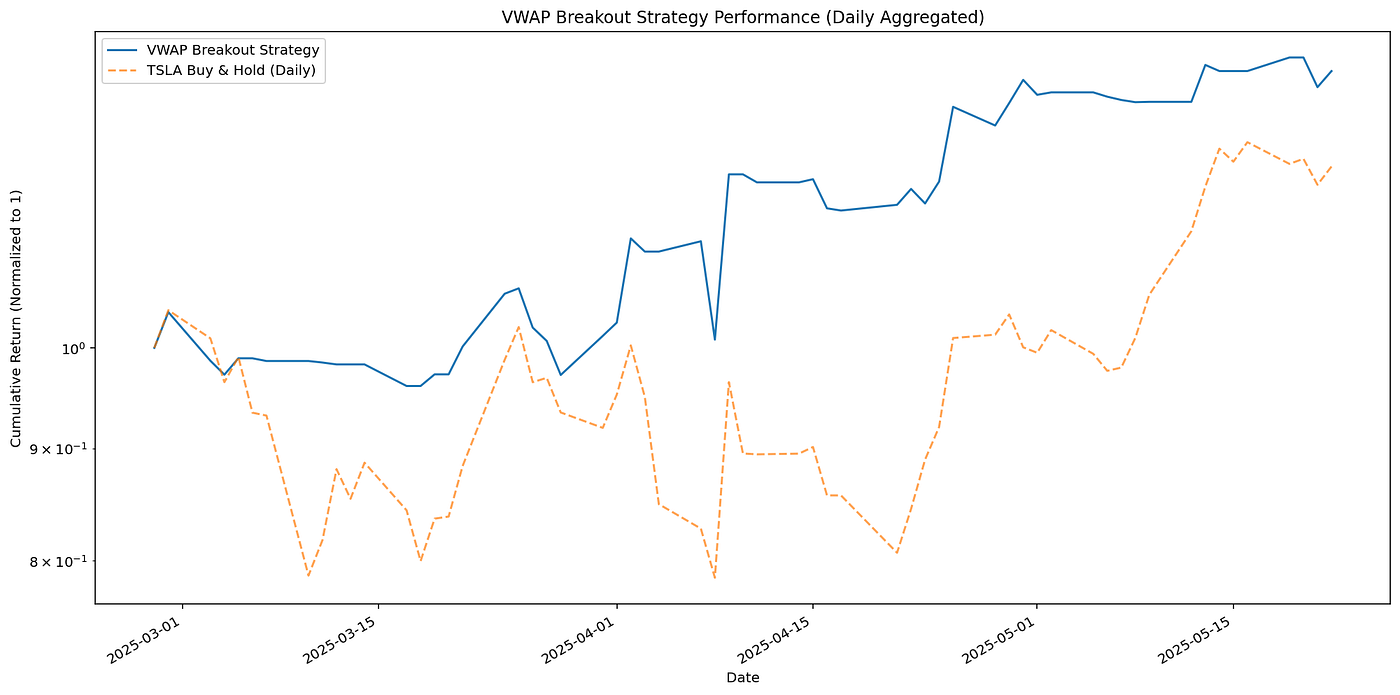

Intraday trading offers a dynamic arena for capturing short-term price movements. Success often hinges on identifying reliable signals that indicate a potential shift in market sentiment with enough conviction to act upon. One popular approach combines the Volume Weighted Average Price (VWAP) as a key benchmark with volume analysis to pinpoint potentially strong breakout opportunities.

This article explores the VWAP Breakout with Volume Confirmation strategy, detailing its components, the rationale behind it, and how key parts can be implemented.

Smarter Investing Starts with Smarter News

The Daily Upside helps 1M+ investors cut through the noise with expert insights. Get clear, concise, actually useful financial news. Smarter investing starts in your inbox—subscribe free.

Understanding the Core Components

At the heart of this strategy lie three critical elements:

VWAP (Volume Weighted Average Price):

VWAP represents the average price an asset has traded at throughout the day, weighted by the volume at each price level. It’s calculated fresh each trading day, typically accumulating from the market open.

Why it matters: Many institutional traders use VWAP as a benchmark for execution quality. It can also act as a dynamic level of support or resistance during the trading day. For intraday traders, it provides a “fair value” reference based on actual trading activity.

Price Breakout Above VWAP:

When an asset’s price moves and closes decisively above its current VWAP, it can signal a shift in intraday control towards buyers. This suggests that, on average, participants are now willing to transact at higher levels than the volume-weighted average established so far in the session.

Volume Surge Confirmation:

A price breakout, on its own, can sometimes be a false alarm (a “fakeout”). Volume is the key to validating the strength and conviction behind the move.

Why it matters: A breakout above VWAP accompanied by a significant surge in trading volume suggests strong buying interest and participation. This increases the probability that the breakout is genuine and might have enough momentum to continue. Conversely, a breakout on low volume is often viewed with skepticism.

The Strategy Logic: Step-by-Step

This strategy operates on an intraday basis (e.g., using 5-minute, 15-minute, or hourly bars). The core logic is to go long when a specific set of conditions are met:

1. Calculate Daily VWAP: As each new intraday bar forms, the VWAP is updated. It’s crucial that this calculation resets at the beginning of each trading day.

For those using Python and pandas, here’s how a daily resetting VWAP might be calculated for an intraday DataFrame df_day:

Python

# Assuming df_day is a pandas DataFrame for a single day's intraday data

# with 'High', 'Low', 'Close', 'Volume' columns.

typical_price = (df_day['High'] + df_day['Low'] + df_day['Close']) / 3

tp_x_volume = typical_price * df_day['Volume']

df_day['VWAP'] = tp_x_volume.cumsum() / df_day['Volume'].cumsum()

# Handle potential division by zero if initial volumes are zero

df_day['VWAP'].fillna(method='ffill', inplace=True)Typically, you’d apply such a function to data grouped by each trading day.

2. Monitor Volume Activity: Calculate a rolling moving average of volume to establish a baseline for “normal” volume.

Python

# Assuming df_intraday has a 'Volume' column

volume_ma_lookback = 20 # Example: 20-bar moving average

df_intraday['Volume_MA'] = df_intraday['Volume'].rolling(window=volume_ma_lookback).mean()3. Identify Entry Conditions (Long):

A long entry signal is generated on an intraday bar if both of the following conditions are met:

Price Condition: The bar’s closing price is above the current VWAP.

Volume Condition: The volume for that bar is significantly greater than its recent moving average (e.g., 1.5x or 2.0x the average). Combining these in Python:

Python

# Assuming df_intraday has 'Close', 'VWAP', 'Volume', 'Volume_MA'

# volume_surge_factor = 1.5 # Example factor

df_intraday['Price_Above_VWAP'] = df_intraday['Close'] > df_intraday['VWAP']

df_intraday['Volume_Surge'] = df_intraday['Volume'] > (df_intraday['Volume_MA'] * volume_surge_factor)

df_intraday['Entry_Signal_Long'] = df_intraday['Price_Above_VWAP'] & \

df_intraday['Volume_Surge']4. Trade Execution and Management (Simplified):

Entry: Upon a valid

Entry_Signal_Long, a long position is initiated (e.g., at the close of the signal bar or open of the next bar).One Trade Per Day: To avoid over-trading or acting on minor subsequent crosses, a common rule is to take only the first valid entry signal per day.

Exit: The exit rule can vary. For simplicity, a common approach for intraday strategies is to exit all positions at the end of the trading day (EOD). More advanced exits could involve profit targets, stop-losses, or the price closing back below VWAP.

Why This Combination Works: The Rationale

The strength of this strategy lies in its logical combination of indicators:

VWAP as a Dynamic Baseline: Unlike fixed support/resistance levels, VWAP is dynamic and reflects the ongoing battle between buyers and sellers throughout the day, weighted by actual transaction volume.

Breakout as Initial Interest: A close above VWAP is the first hint that buyers might be gaining control.

Volume as Conviction: The volume surge acts as a powerful filter. It suggests that the move above VWAP isn’t just random noise but is backed by significant market participation and conviction, increasing the odds of follow-through. It helps differentiate between a tentative probe above VWAP and a more decisive shift in sentiment.

This strategy aims to capture strong intraday momentum bursts that are validated by institutional or broad market interest, as indicated by volume.

Considerations and Limitations

Data Requirements: Reliable, clean intraday OHLCV (Open, High, Low, Close, Volume) data is essential.

yfinancecan provide this, but historical depth for short intervals (e.g., 1-minute, 5-minute) is often limited (typically the last 7-60 days).Parameter Sensitivity: The choice of intraday bar interval, the

volume_ma_lookbackperiod, and thevolume_surge_factorare crucial parameters that need to be tested and potentially optimized for the specific asset and market conditions.Whipsaws: Like all breakout strategies, this approach can still be prone to “whipsaws” — where price breaks out, triggers a trade, and then quickly reverses.

Market Regimes: The strategy’s effectiveness can vary. It might perform well when there’s clear intraday directionality and volume participation but could struggle in extremely choppy, low-volume, or news-driven erratic markets.

Transaction Costs: Intraday strategies can involve more frequent trading, so transaction costs (brokerage fees, slippage) must be carefully considered as they can significantly impact net profitability.

Exit Strategy: The choice of exit strategy is just as important as the entry and can greatly influence overall results. The EOD exit used in the illustrative code is just one simple option.

Conclusion

The VWAP Breakout with Volume Confirmation strategy offers a systematic and logical approach to intraday trading. By anchoring decisions to the volume-weighted average price and demanding strong volume to validate breakouts, traders aim to filter out weaker signals and participate in moves with higher conviction. While no strategy is foolproof, this combination provides a robust framework that, with careful parameterization and risk management, can be a valuable tool in an intraday trader’s arsenal. As always, thorough backtesting and adaptation to specific market characteristics are key to its successful application.