In partnership with

The Supply Chain Crisis Is Escalating — But This Tech Startup Keeps Winning

Global supply chain chaos is intensifying. Major retailers warn of holiday shortages, and tech giants are slashing forecasts as parts dry up.

But while others scramble, one smart home innovator is thriving.

Their strategic move to manufacturing outside China has kept production running smoothly — driving 200% year-over-year growth, even as the industry stalls.

This foresight is no accident. The same leadership team that saw the supply chain storm coming has already expanded into over 120 BestBuy locations, with talks underway to add Walmart and Home Depot.

At just $1.90 per share, this resilient tech startup offers rare stability in uncertain times. As investors flee vulnerable companies, this window is closing fast.

Past performance is not indicative of future results. Email may contain forward-looking statements. See US Offering for details. Informational purposes only.

🚀 Your Investing Journey Just Got Better: Premium Subscriptions Are Here! 🚀

It’s been 4 months since we launched our premium subscription plans at GuruFinance Insights, and the results have been phenomenal! Now, we’re making it even better for you to take your investing game to the next level. Whether you’re just starting out or you’re a seasoned trader, our updated plans are designed to give you the tools, insights, and support you need to succeed.

Here’s what you’ll get as a premium member:

Exclusive Trading Strategies: Unlock proven methods to maximize your returns.

In-Depth Research Analysis: Stay ahead with insights from the latest market trends.

Ad-Free Experience: Focus on what matters most—your investments.

Monthly AMA Sessions: Get your questions answered by top industry experts.

Coding Tutorials: Learn how to automate your trading strategies like a pro.

Masterclasses & One-on-One Consultations: Elevate your skills with personalized guidance.

Our three tailored plans—Starter Investor, Pro Trader, and Elite Investor—are designed to fit your unique needs and goals. Whether you’re looking for foundational tools or advanced strategies, we’ve got you covered.

Don’t wait any longer to transform your investment strategy. The last 4 months have shown just how powerful these tools can be—now it’s your turn to experience the difference.

Made with Python

The Power of Adaptive Leverage in Trading

Many traders face a dilemma: shorting individual stocks carries substantial risks from unexpected news, earnings surprises, and volatility spikes. Yet a strict long-only approach may sacrifice potential returns during market downturns.

What if we could enhance a long-only strategy with tactical leverage?

The Multi-Regime Adaptive Leverage Strategy (MRALS) offers precisely this solution: applying varying levels of leverage (0x to 3x) based on market conditions while maintaining a long-only discipline.

Smarter Investing Starts with Smarter News

The Daily Upside helps 1M+ investors cut through the noise with expert insights. Get clear, concise, actually useful financial news. Smarter investing starts in your inbox—subscribe free.

MRALS Strategy Overview

MRALS combines three key innovations:

Adaptive leverage based on market regimes: Applying 0–3x leverage depending on volatility conditions.

Yang-Zhang volatility measurement: Using superior volatility detection that captures overnight gaps.

Realistic trade execution: Generating signals at market close but executing at the next day’s open.

Rather than attempting to short during downturns, MRALS shifts to cash (0x exposure) in high-volatility environments while amplifying exposure (up to 3x) during favorable conditions.

Strategy Components

The strategy classifies market conditions into four distinct regimes:

Aggressive (3x leverage): Low volatility + strong bullish trend + normal VIX term structure.

Bullish (2x leverage): Positive trend with moderate volatility.

Moderate (1x leverage): Neutral conditions.

Defensive (0x leverage): High volatility or bearish signals.

A hybrid oscillator combining price momentum and volatility metrics generates entry and exit signals, while the Yang-Zhang volatility model provides more accurate risk assessment than traditional methods.

Here is the code, so you can modify it or backtest it:

import pandas as pd

import numpy as np

import yfinance as yf

import matplotlib.pyplot as plt

from matplotlib.gridspec import GridSpec

def fetch_data(ticker, start_date, end_date=None):

"""Downloads data including OHLC and the actual VIX and VIX3M indices"""

# Data download

data = yf.download(ticker, start=start_date, end=end_date)

vix = yf.download("^VIX", start=start_date, end=end_date)['Close']

vix3m = yf.download("^VIX3M", start=start_date, end=end_date)['Close']

df = pd.DataFrame(index=data.index)

df['Open'] = data['Open']

df['High'] = data['High']

df['Low'] = data['Low']

df['Close'] = data['Close']

df['Volume'] = data['Volume']

df['VIX'] = vix

df['VIX3M'] = vix3m # Use the actual VIX3M instead of the synthetic version

df['VIX_Ratio'] = df['VIX'] / df['VIX3M']

return df.dropna()

def calculate_yang_zhang_volatility(data, window=21):

"""Calculates Yang-Zhang volatility"""

open_price = data['Open']

high_price = data['High']

low_price = data['Low']

close_price = data['Close']

# Logarithmic calculations

log_ho = np.log(high_price / open_price)

log_lo = np.log(low_price / open_price)

log_oc = np.log(close_price / open_price)

log_co = np.log(open_price / close_price.shift(1))

# Volatility components

rs = log_ho * (log_ho - log_oc) + log_lo * (log_lo - log_oc)

close_vol = log_oc**2

open_vol = log_co**2

# Moving values

rs_roll = rs.rolling(window=window).mean()

close_roll = close_vol.rolling(window=window).mean()

open_roll = open_vol.rolling(window=window).mean()

# Optimal k factor for Yang-Zhang

k = 0.34 / (1.34 + (window + 1) / (window - 1))

# YZ Volatility

yz_vol = np.sqrt(open_roll + k * close_roll + (1 - k) * rs_roll)

# Annualize (multiply by sqrt(252))

return yz_vol * np.sqrt(252)

def calculate_oscillator(data):

"""Creates a hybrid oscillator"""

# Momentum component (differential EMA)

ema_fast = data['Close'].ewm(span=8, adjust=False).mean()

ema_slow = data['Close'].ewm(span=21, adjust=False).mean()

momentum = ((ema_fast / ema_slow) - 1) * 100

# Relative strength component

rel_strength = data['Close'].pct_change(21) - data['Close'].pct_change(21).rolling(252).mean()

rel_strength = rel_strength / rel_strength.rolling(63).std().fillna(0.0001)

# Volatility component

vol_ratio = data['VIX_Ratio'] - data['VIX_Ratio'].rolling(21).mean()

vol_ratio = vol_ratio / vol_ratio.rolling(63).std().fillna(0.0001)

# Final oscillator (weighted combination)

oscillator = (0.5 * momentum) + (0.3 * rel_strength) - (0.2 * vol_ratio)

# Smoothing to reduce noise

oscillator_smooth = oscillator.ewm(span=5, adjust=False).mean()

return oscillator_smooth

def detect_market_regime(data, yz_vol, oscillator):

"""Detects the market regime and determines the leverage factor"""

# Classify volatility

vol_percentile = yz_vol.rolling(252).rank(pct=True).fillna(0.5)

low_vol = vol_percentile < 0.2

high_vol = vol_percentile > 0.8

# Price trend

price_trend = data['Close'] > data['Close'].rolling(50).mean()

price_momentum = data['Close'].pct_change(63) > 0

# VIX indicator

vix_contango = data['VIX_Ratio'] < 0.9 # VIX < VIX3M (normal market)

vix_backwardation = data['VIX_Ratio'] > 1.1 # VIX > VIX3M (market stress)

# Oscillator signal

oscillator_bullish = oscillator > 0.5

oscillator_bearish = oscillator < -0.5

# Determine regime

regime = pd.Series(index=data.index, dtype='object')

# Condition combinations

regime[oscillator_bullish & low_vol & price_trend & vix_contango] = 'Aggressive' # 3x

regime[oscillator_bullish & price_trend & ~high_vol] = 'Bullish' # 2x

regime[(~oscillator_bearish & ~oscillator_bullish) |

(price_momentum & ~high_vol)] = 'Moderate' # 1x

regime[oscillator_bearish | high_vol | vix_backwardation] = 'Defensive' # 0x

# Fill NA values with 'Moderate'

regime = regime.fillna('Moderate')

# Convert to leverage factor

leverage_factor = pd.Series(index=data.index)

leverage_factor[regime == 'Aggressive'] = 3.0

leverage_factor[regime == 'Bullish'] = 2.0

leverage_factor[regime == 'Moderate'] = 1.0

leverage_factor[regime == 'Defensive'] = 0.0

return regime, leverage_factor

def generate_signals(data, oscillator, leverage_factor):

"""Generates signals based on the oscillator and market regime"""

signals = pd.DataFrame(index=data.index)

signals['Close'] = data['Close']

signals['Open'] = data['Open']

signals['Oscillator'] = oscillator

signals['Regime'] = leverage_factor

# Initialize columns

signals['Signal'] = 0

signals['Entry'] = 0

signals['Exit'] = 0

signals['Position'] = 0

signals['Leverage'] = 0

# Moving average of the oscillator for crossover

oscillator_ma = oscillator.rolling(window=13).mean()

# Generate signals

for i in range(13, len(signals)):

# Current and previous values

curr_osc = oscillator.iloc[i]

prev_osc = oscillator.iloc[i-1]

curr_ma = oscillator_ma.iloc[i]

prev_ma = oscillator_ma.iloc[i-1]

curr_lev = leverage_factor.iloc[i]

# Entry signal: crossover or regime improvement

if ((prev_osc <= prev_ma and curr_osc > curr_ma) or

(signals['Position'].iloc[i-1] == 0 and curr_lev >= 1.0 and

signals['Leverage'].iloc[i-1] < 1.0)):

signals.loc[signals.index[i], 'Signal'] = 1

signals.loc[signals.index[i], 'Entry'] = 1

# Exit signal: crossunder or defensive regime

elif ((prev_osc >= prev_ma and curr_osc < curr_ma) or

(signals['Position'].iloc[i-1] > 0 and curr_lev == 0)):

signals.loc[signals.index[i], 'Signal'] = -1

signals.loc[signals.index[i], 'Exit'] = 1

# Position adjustment if leverage changes without exiting

elif (signals['Position'].iloc[i-1] > 0 and

curr_lev != signals['Leverage'].iloc[i-1] and

curr_lev > 0):

signals.loc[signals.index[i], 'Signal'] = 2 # Adjustment signal

# Calculate position and leverage

if signals['Entry'].iloc[i] == 1:

signals.loc[signals.index[i], 'Position'] = 1

signals.loc[signals.index[i], 'Leverage'] = curr_lev

elif signals['Exit'].iloc[i] == 1:

signals.loc[signals.index[i], 'Position'] = 0

signals.loc[signals.index[i], 'Leverage'] = 0

elif signals['Signal'].iloc[i] == 2: # Adjustment

signals.loc[signals.index[i], 'Position'] = 1

signals.loc[signals.index[i], 'Leverage'] = curr_lev

else:

signals.loc[signals.index[i], 'Position'] = signals['Position'].iloc[i-1]

signals.loc[signals.index[i], 'Leverage'] = signals['Leverage'].iloc[i-1]

return signals

def backtest_strategy(signals, initial_capital=100000):

"""Executes backtest with entry at the next day's open"""

backtest = signals.copy()

# Prepare for backtesting with entry on the next day

backtest['Next_Open'] = backtest['Open'].shift(-1)

# Initialize backtest columns

backtest['Trade_Entry'] = np.nan

backtest['Trade_Exit'] = np.nan

backtest['Trade_Return'] = np.nan

backtest['Strategy_Return'] = 0.0

# Trade tracking

in_position = False

entry_price = 0

entry_date = None

entry_leverage = 0

# Process day by day

for i in range(len(backtest)-1): # Ignore last day

current_date = backtest.index[i]

next_date = backtest.index[i+1]

# Buy signal at close = entry next day

if backtest['Entry'].iloc[i] == 1 and not in_position:

entry_price = backtest['Next_Open'].iloc[i]

entry_date = next_date

entry_leverage = backtest['Leverage'].iloc[i]

in_position = True

backtest.loc[next_date, 'Trade_Entry'] = entry_price

# Sell signal at close = exit next day

elif backtest['Exit'].iloc[i] == 1 and in_position:

exit_price = backtest['Next_Open'].iloc[i]

# Calculate trade return

trade_return = (exit_price / entry_price - 1) * entry_leverage

# Record exit

backtest.loc[next_date, 'Trade_Exit'] = exit_price

backtest.loc[next_date, 'Trade_Return'] = trade_return

# Reset

in_position = False

entry_price = 0

entry_date = None

entry_leverage = 0

# Leverage adjustment (without closing position)

elif backtest['Signal'].iloc[i] == 2 and in_position:

new_leverage = backtest['Leverage'].iloc[i]

entry_leverage = new_leverage

# Calculate daily strategy returns

for i in range(1, len(backtest)-1):

if backtest['Position'].iloc[i] == 1:

# Return from current open to next open

daily_return = backtest['Next_Open'].iloc[i] / backtest['Open'].iloc[i] - 1

leveraged_return = daily_return * backtest['Leverage'].iloc[i]

backtest.loc[backtest.index[i+1], 'Strategy_Return'] = leveraged_return

# Calculate equity curve

backtest['Strategy_Equity'] = (1 + backtest['Strategy_Return'].fillna(0)).cumprod()

# Buy & hold for comparison

backtest['BuyHold_Return'] = backtest['Open'].pct_change()

backtest['BuyHold_Equity'] = (1 + backtest['BuyHold_Return'].fillna(0)).cumprod()

# Drawdowns

backtest['Strategy_Peak'] = backtest['Strategy_Equity'].expanding().max()

backtest['Strategy_Drawdown'] = backtest['Strategy_Equity'] / backtest['Strategy_Peak'] - 1

backtest['BuyHold_Peak'] = backtest['BuyHold_Equity'].expanding().max()

backtest['BuyHold_Drawdown'] = backtest['BuyHold_Equity'] / backtest['BuyHold_Peak'] - 1

return backtest

def calculate_metrics(backtest):

"""Calculates performance metrics"""

# Filter returns

strategy_returns = backtest['Strategy_Return'].dropna()

bh_returns = backtest['BuyHold_Return'].dropna()

trade_returns = backtest['Trade_Return'].dropna()

if len(strategy_returns) == 0:

return {

'Total Return': 0,

'Annual Return': 0,

'Annual Volatility': 0,

'Sharpe Ratio': 0,

'Max Drawdown': 0,

'Number of Trades': 0,

'Win Rate': 0,

'Average Win': 0,

'Average Loss': 0,

'Time in Market': 0,

'Average Exposure': 0,

'BH Total Return': 0,

'BH Annual Return': 0,

'BH Annual Volatility': 0,

'BH Sharpe Ratio': 0,

'BH Max Drawdown': 0

}

# Calculate metrics

metrics = {}

# Total and annual

metrics['Total Return'] = backtest['Strategy_Equity'].iloc[-1] - 1

years = len(backtest) / 252

metrics['Annual Return'] = (1 + metrics['Total Return']) ** (1/years) - 1

# Risk

metrics['Annual Volatility'] = strategy_returns.std() * np.sqrt(252)

metrics['Sharpe Ratio'] = metrics['Annual Return'] / metrics['Annual Volatility'] if metrics['Annual Volatility'] > 0 else 0

metrics['Max Drawdown'] = backtest['Strategy_Drawdown'].min()

# Trade statistics

metrics['Number of Trades'] = len(trade_returns)

metrics['Win Rate'] = (trade_returns > 0).mean() if len(trade_returns) > 0 else 0

metrics['Average Win'] = trade_returns[trade_returns > 0].mean() if len(trade_returns[trade_returns > 0]) > 0 else 0

metrics['Average Loss'] = trade_returns[trade_returns < 0].mean() if len(trade_returns[trade_returns < 0]) > 0 else 0

# Time in market

metrics['Time in Market'] = (backtest['Position'] > 0).mean()

# Average exposure (considering leverage)

metrics['Average Exposure'] = backtest['Leverage'].mean()

# Buy & Hold

metrics['BH Total Return'] = backtest['BuyHold_Equity'].iloc[-1] - 1

metrics['BH Annual Return'] = (1 + metrics['BH Total Return']) ** (1/years) - 1

metrics['BH Annual Volatility'] = bh_returns.std() * np.sqrt(252)

metrics['BH Sharpe Ratio'] = metrics['BH Annual Return'] / metrics['BH Annual Volatility'] if metrics['BH Annual Volatility'] > 0 else 0

metrics['BH Max Drawdown'] = backtest['BuyHold_Drawdown'].min()

return metrics

def plot_results(backtest, yz_vol, oscillator, regime, metrics):

"""Visualizes the strategy results"""

# Configuration

fig = plt.figure(figsize=(15, 18))

gs = GridSpec(4, 2, height_ratios=[2, 1, 1, 1], hspace=0.4, wspace=0.3)

# 1. Price and signals

ax1 = fig.add_subplot(gs[0, :])

ax1.plot(backtest.index, backtest['Close'], color='blue', label='Price', alpha=0.7)

# Mark entries and exits

entries = backtest.dropna(subset=['Trade_Entry'])

exits = backtest.dropna(subset=['Trade_Exit'])

# Differentiate entries by leverage

if len(entries) > 0:

for i, row in entries.iterrows():

marker_size = 50 + 50 * row['Leverage'] # Size based on leverage

ax1.scatter(i, row['Trade_Entry'], color='green', marker='^',

s=marker_size, alpha=0.7)

if len(exits) > 0:

ax1.scatter(exits.index, exits['Trade_Exit'], color='red', marker='v',

s=100, alpha=0.7, label='Exit')

ax1.set_title('Price with Trading Signals', fontsize=14)

ax1.set_ylabel('Price', fontsize=12)

ax1.legend(loc='upper left')

ax1.grid(True, alpha=0.3)

# 2. Oscillator

ax2 = fig.add_subplot(gs[1, 0:1])

ax2.plot(backtest.index, oscillator, label='Oscillator', color='purple')

ax2.plot(backtest.index, oscillator.rolling(13).mean(), label='MA(13)',

color='orange', linestyle='--')

ax2.axhline(y=0, color='black', linestyle='-', alpha=0.3)

ax2.set_title('Hybrid Oscillator', fontsize=14)

ax2.set_ylabel('Value', fontsize=12)

ax2.legend()

ax2.grid(True, alpha=0.3)

# 3. Yang-Zhang Volatility

ax3 = fig.add_subplot(gs[1, 1:2])

ax3.plot(backtest.index, yz_vol, label='YZ Volatility', color='red')

ax3.set_title('Yang-Zhang Annualized Volatility', fontsize=14)

ax3.set_ylabel('Volatility', fontsize=12)

ax3.legend()

ax3.grid(True, alpha=0.3)

# 4. Exposure / Leverage

ax4 = fig.add_subplot(gs[2, :])

ax4.plot(backtest.index, backtest['Leverage'], label='Leverage Factor',

color='orange', linewidth=2)

ax4.set_title('Exposure / Leverage', fontsize=14)

ax4.set_ylabel('Factor (x)', fontsize=12)

ax4.set_ylim(0, 3.5)

ax4.legend()

ax4.grid(True, alpha=0.3)

# 5. Equity Curves

ax5 = fig.add_subplot(gs[3, :])

ax5.plot(backtest.index, backtest['Strategy_Equity'], label='MRALS Strategy',

color='blue', linewidth=2)

ax5.plot(backtest.index, backtest['BuyHold_Equity'], label='Buy & Hold',

color='gray', linestyle='--', alpha=0.7)

ax5.set_title('Equity Curves', fontsize=14)

ax5.set_ylabel('Equity (Normalized)', fontsize=12)

ax5.set_xlabel('Date', fontsize=12)

ax5.legend()

ax5.grid(True, alpha=0.3)

# Add metrics table

metrics_text = (

f"MRALS STRATEGY vs BUY & HOLD\n"

f"='='='='='='='='='='='='='='\n"

f"Total Return: {metrics['Total Return']*100:.2f}% vs {metrics['BH Total Return']*100:.2f}%\n"

f"Annual Return: {metrics['Annual Return']*100:.2f}% vs {metrics['BH Annual Return']*100:.2f}%\n"

f"Volatility: {metrics['Annual Volatility']*100:.2f}% vs {metrics['BH Annual Volatility']*100:.2f}%\n"

f"Sharpe Ratio: {metrics['Sharpe Ratio']:.2f} vs {metrics['BH Sharpe Ratio']:.2f}\n"

f"Maximum Drawdown: {metrics['Max Drawdown']*100:.2f}% vs {metrics['BH Max Drawdown']*100:.2f}%\n\n"

f"ADDITIONAL STATISTICS\n"

f"='='='='='='='='='='='='='\n"

f"Number of Trades: {int(metrics['Number of Trades'])}\n"

f"Win Rate: {metrics['Win Rate']*100:.2f}%\n"

f"Average Win: {metrics['Average Win']*100:.2f}%\n"

f"Average Loss: {metrics['Average Loss']*100:.2f}%\n"

f"Time in Market: {metrics['Time in Market']*100:.2f}%\n"

f"Average Exposure: {metrics['Average Exposure']:.2f}x"

)

# Add text box with metrics

props = dict(boxstyle='round', facecolor='wheat', alpha=0.4)

ax5.text(0.02, 0.02, metrics_text, transform=ax5.transAxes, fontsize=10,

verticalalignment='bottom', horizontalalignment='left', bbox=props)

plt.tight_layout()

plt.show()

def run_strategy(ticker='SPY', start_date='2015-01-01', end_date=None):

"""Executes the complete strategy"""

# Download data

data = fetch_data(ticker, start_date, end_date)

# Calculate Yang-Zhang volatility

yz_vol = calculate_yang_zhang_volatility(data)

# Calculate hybrid oscillator

oscillator = calculate_oscillator(data)

# Detect market regime and leverage factor

regime, leverage_factor = detect_market_regime(data, yz_vol, oscillator)

# Generate signals

signals = generate_signals(data, oscillator, leverage_factor)

# Execute backtest

backtest = backtest_strategy(signals)

# Calculate metrics

metrics = calculate_metrics(backtest)

# Visualize results

plot_results(backtest, yz_vol, oscillator, regime, metrics)

return backtest, metrics

# Example usage

backtest, metrics = run_strategy('SPY', '2018-01-01')Risk Management Focus

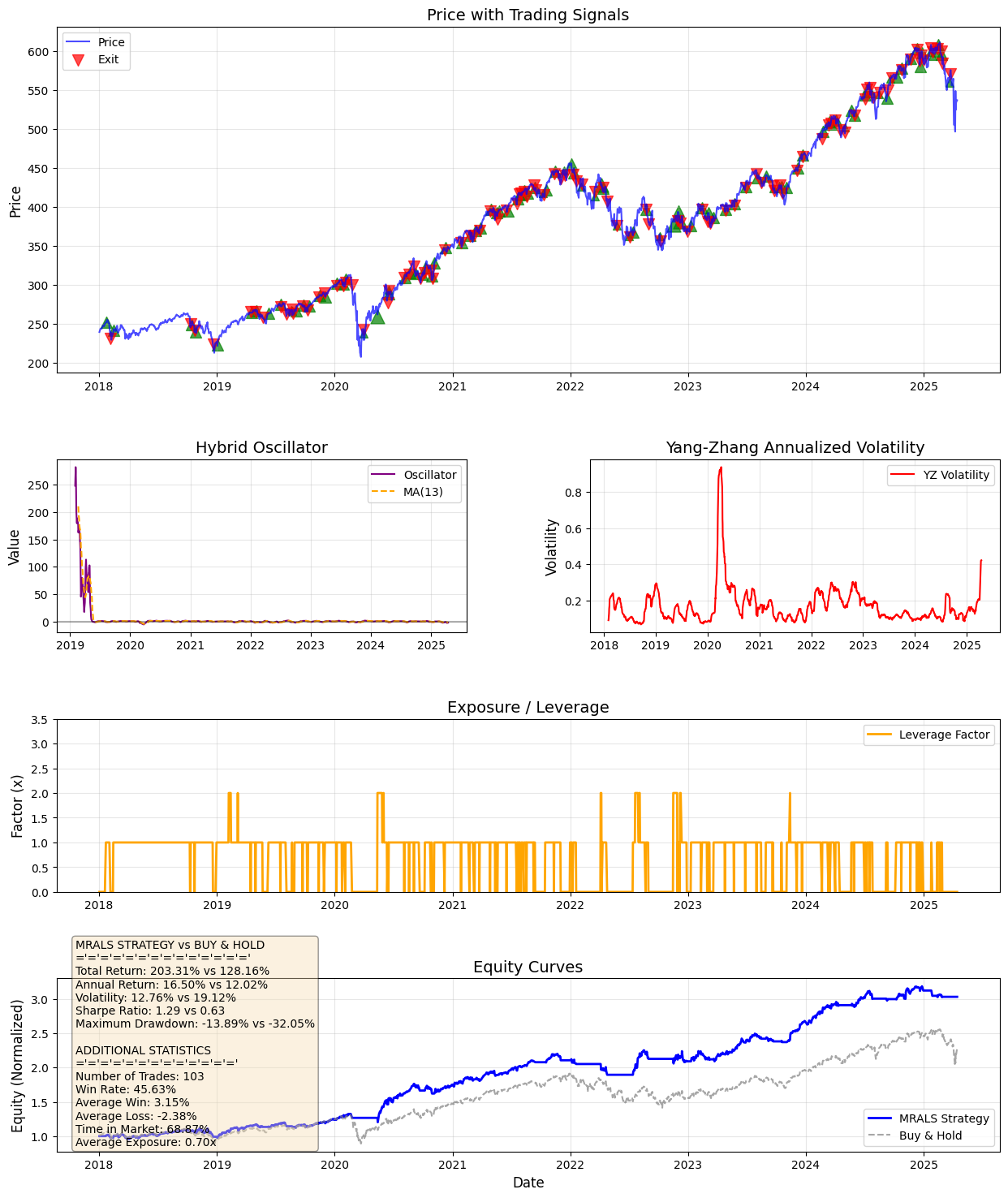

The strategy completed 103 trades with a 45.63% win rate. While this may appear modest, the average winning trade (+3.15%) exceeded the average losing trade (-2.38%), creating positive expectancy.

Most importantly, MRALS spent only 68.67% of time in the market, moving to cash during unfavorable conditions. The average leverage of 0.70x, below the neutral 1.0x position, demonstrates the strategy’s conservative approach to risk management.

Conclusion

MRALS demonstrates that a long-only approach can be significantly enhanced through tactical leverage without resorting to shorting. By applying greater exposure during favorable conditions and stepping aside during turbulent periods, the strategy achieved 59% higher returns than buy & hold while dramatically reducing volatility and drawdowns.

The combination of Yang-Zhang volatility measurement and adaptive leverage provides a compelling framework for investors who want to remain long-only but seek enhanced returns beyond traditional buy-and-hold approaches.