In partnership with

There’s a reason 400,000 professionals read this daily.

Join The AI Report, trusted by 400,000+ professionals at Google, Microsoft, and OpenAI. Get daily insights, tools, and strategies to master practical AI skills that drive results.

🚀 Your Investing Journey Just Got Better: Premium Subscriptions Are Here! 🚀

It’s been 4 months since we launched our premium subscription plans at GuruFinance Insights, and the results have been phenomenal! Now, we’re making it even better for you to take your investing game to the next level. Whether you’re just starting out or you’re a seasoned trader, our updated plans are designed to give you the tools, insights, and support you need to succeed.

Here’s what you’ll get as a premium member:

Exclusive Trading Strategies: Unlock proven methods to maximize your returns.

In-Depth Research Analysis: Stay ahead with insights from the latest market trends.

Ad-Free Experience: Focus on what matters most—your investments.

Monthly AMA Sessions: Get your questions answered by top industry experts.

Coding Tutorials: Learn how to automate your trading strategies like a pro.

Masterclasses & One-on-One Consultations: Elevate your skills with personalized guidance.

Our three tailored plans—Starter Investor, Pro Trader, and Elite Investor—are designed to fit your unique needs and goals. Whether you’re looking for foundational tools or advanced strategies, we’ve got you covered.

Don’t wait any longer to transform your investment strategy. The last 4 months have shown just how powerful these tools can be—now it’s your turn to experience the difference.

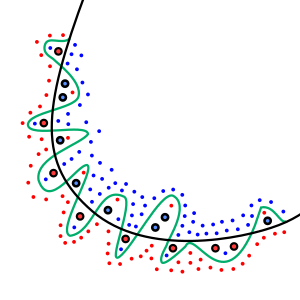

Overfitting in machine learning

In the intricate world of algorithmic trading, the pursuit of creating the ‘perfect’ model often leads to a ubiquitous problem: overfitting. This phenomenon, akin to memorizing the answers to an exam rather than understanding the concepts, can have serious implications for traders. Let’s delve deeper.

Smart Money, Smart Machines

Dubbed "the rocket fuel of AI" by Wired, this innovation is causing a stir on Wall Street. With projections hitting $80 trillion – that's 41 Amazons – the potential is huge. But here's the deal: sharp investors who are ahead of the game have the opportunity to invest in a technology poised for domination. Thanks to The Motley Fool, you can access the full story in this exclusive report.

1. What is Overfitting in the Context of Algo Trading?

Overfitting occurs when a trading algorithm is too closely tailored to historical market data, capturing not only the underlying patterns but also the market noise. Such an over-optimized strategy might show stellar backtested results but can perform poorly in live trading.

Example:

Imagine a trading model built on the past 10 years of stock price data. If it’s developed to capture every minute fluctuation, it might fail when faced with new, unforeseen market conditions.

2. Causes of Overfitting in Algo Trading

Complex Models: Using overly complex models for relatively simple patterns in data.

Limited Data: Training on a small dataset and not validating on out-of-sample data.

Noise Capture: Misinterpreting market noise as genuine trading signals.

3. Detecting Overfitting

Performance Discrepancy:

A clear indicator is when there’s a vast difference between backtested results and live trading performance.

Learning Curves:

By plotting the model’s performance on both training and validation datasets, overfitting becomes evident when the training performance continues to improve while validation performance stagnates or deteriorates.

import numpy as np

import matplotlib.pyplot as plt

from sklearn.model_selection import learning_curve

# Sample code to plot learning curves

def plot_learning_curve(estimator, title, X, y, ylim=None, cv=None, n_jobs=None, train_sizes=np.linspace(.1, 1.0, 5)):

plt.figure()

plt.title(title)

if ylim is not None:

plt.ylim(*ylim)

plt.xlabel("Training examples")

plt.ylabel("Score")

train_sizes, train_scores, test_scores = learning_curve(estimator, X, y, cv=cv, n_jobs=n_jobs, train_sizes=train_sizes)

train_scores_mean = np.mean(train_scores, axis=1)

train_scores_std = np.std(train_scores, axis=1)

test_scores_mean = np.mean(test_scores, axis=1)

test_scores_std = np.std(test_scores, axis=1)

plt.grid()

plt.fill_between(train_sizes, train_scores_mean - train_scores_std, train_scores_mean + train_scores_std, alpha=0.1, color="r")

plt.fill_between(train_sizes, test_scores_mean - test_scores_std, test_scores_mean + test_scores_std, alpha=0.1, color="g")

plt.plot(train_sizes, train_scores_mean, 'o-', color="r", label="Training score")

plt.plot(train_sizes, test_scores_mean, 'o-', color="g", label="Cross-validation score")

plt.legend(loc="best")

return plt4. Solutions to Overfitting in Algo Trading

Simplifying the Model:

Sometimes, less is more. Opt for simpler models unless the complexity is justified.

Regularization:

This technique adds a penalty to the loss function, discouraging overly complex models. In the context of regression, methods like Ridge and Lasso can be used.

from sklearn.linear_model import Ridge

# Ridge Regression with alpha as the regularization strength

ridge = Ridge(alpha=1.0)

ridge.fit(X_train, y_train)Expanding Data:

The more data, the merrier. Gathering more historical data or incorporating other related datasets can help.

Out-of-sample Testing:

Always validate the algorithm’s performance on out-of-sample data, which hasn’t been used during the training process.

Walk-forward Validation:

This rolling-forward testing approach uses a dynamic window to train and validate, making the model more adaptable to new data.

# Sample code for walk-forward validation

for i in range(len(test)):

train, test_data = data[i:len(train)+i], data[len(train)+i]

model.fit(train)

predictions.append(model.predict(test_data))Ensemble Methods:

Combining multiple models can help in reducing overfitting. Methods like bagging and boosting can be particularly effective.

While the allure of high backtested returns can be tempting, it’s crucial for traders to be aware of the pitfalls of overfitting. By understanding its causes and applying robust validation techniques, one can navigate the choppy waters of algorithmic trading with greater confidence.