In partnership with

Apple's New Smart Display Confirms What This Startup Knew All Along

Apple has entered the smart home race with its new Smart Display, firing a $158B signal that connected homes are the future.

When Apple moves in, it doesn’t just join the market — it transforms it.

One company has been quietly preparing for this moment.

Their smart shade technology already works across every major platform, perfectly positioned to capture the wave of new consumers Apple will bring.

While others scramble to catch up, this startup is already shifting production from China to its new facility in the Philippines — built for speed and ready to meet surging demand as Apple’s marketing machine drives mass adoption.

With 200% year-over-year growth and distribution in over 120 Best Buy locations, this company isn’t just ready for Apple’s push — they’re set to thrive from it.

Shares in this tech company are open at just $1.90.

Apple’s move is accelerating the entire sector. Don’t miss this window.

Past performance is not indicative of future results. Email may contain forward-looking statements. See US Offering for details. Informational purposes only.

🚀 Your Investing Journey Just Got Better: Premium Subscriptions Are Here! 🚀

It’s been 4 months since we launched our premium subscription plans at GuruFinance Insights, and the results have been phenomenal! Now, we’re making it even better for you to take your investing game to the next level. Whether you’re just starting out or you’re a seasoned trader, our updated plans are designed to give you the tools, insights, and support you need to succeed.

Here’s what you’ll get as a premium member:

Exclusive Trading Strategies: Unlock proven methods to maximize your returns.

In-Depth Research Analysis: Stay ahead with insights from the latest market trends.

Ad-Free Experience: Focus on what matters most—your investments.

Monthly AMA Sessions: Get your questions answered by top industry experts.

Coding Tutorials: Learn how to automate your trading strategies like a pro.

Masterclasses & One-on-One Consultations: Elevate your skills with personalized guidance.

Our three tailored plans—Starter Investor, Pro Trader, and Elite Investor—are designed to fit your unique needs and goals. Whether you’re looking for foundational tools or advanced strategies, we’ve got you covered.

Don’t wait any longer to transform your investment strategy. The last 4 months have shown just how powerful these tools can be—now it’s your turn to experience the difference.

Introduction

The question of market timing has challenged investors for generations. While perfect market timing remains elusive, sophisticated indicators can provide valuable insights into market sentiment – that ephemeral mix of fear, greed, and rationality that often drives price action more than fundamentals.

In this article, I’ll walk through the development of a proprietary market sentiment indicator that combines three powerful market forces: Yang-Zhang volatility, VIX term structure, and sector rotation dynamics. The result is an intuitive “sentiment clock” that normalizes complex market signals into an easy-to-interpret 0–100 scale, with built-in risk management via Conditional Drawdown at Risk (CDaR).

Hands Down Some Of The Best Credit Cards Of 2025

Pay No Interest Until Nearly 2027 AND Earn 5% Cash Back

The Three Pillars of Market Sentiment

Our sentiment indicator rests on three fundamental pillars that, when combined, provide a comprehensive view of market psychology:

1. Yang-Zhang Volatility

Unlike basic volatility measures that only consider closing prices, Yang-Zhang volatility incorporates opening, high, low, and closing prices to capture both overnight jumps and intraday price action. This sophisticated approach provides a more nuanced view of market turbulence.

Yang-Zhang volatility combines three components:

Overnight volatility (close-to-open)

Open-to-close volatility

Rogers-Satchell volatility (which captures directional price movement)

In our indicator, lower Yang-Zhang volatility contributes positively to the sentiment score, as markets tend to rise more steadily during periods of calm.

2. VIX/VIX3M Ratio

The relationship between short-term (VIX) and medium-term (VIX3M) implied volatility offers fascinating insights into market expectations.

When VIX > VIX3M (ratio > 1): Markets anticipate higher short-term volatility relative to medium-term volatility, typically signaling immediate stress or fear

- When VIX < VIX3M (ratio < 1): Markets expect relative calm in the near term, often associated with complacency or optimism

Our indicator inverts this ratio so that lower values (indicating market stress) contribute negatively to sentiment, while higher values (indicating market calm) contribute positively.

3. Cyclical vs. Defensive Sector Ratio

Perhaps the most revealing insight comes from how investors rotate between cyclical sectors (that thrive during economic expansion) and defensive sectors (that outperform during economic uncertainty):

Cyclical sectors: Technology (XLK), Consumer Discretionary (XLY), Industrials (XLI)

Defensive sectors: Consumer Staples (XLP), Utilities (XLU), Healthcare (XLV)

When investors favor cyclical sectors over defensive ones, it signals confidence in economic growth. Conversely, rotation into defensive sectors often indicates concern about future economic prospects.

Our indicator tracks this ratio, with higher values (cyclical outperformance) contributing positively to the sentiment score.

The Market Sentiment Clock

The innovation in our approach lies in combining these three components into a single, intuitive meter normalized on a 0–100 scale – what we call the “Market Sentiment Clock.”

The sentiment scale divides into five distinct zones:

0–20: Extreme Fear

20–40: Fear

40–60: Neutral

60–80: Optimism

80–100: Euphoria

This normalization occurs through a percentile-based approach using a rolling historical window (typically 252 trading days). This adaptive normalization ensures the sentiment gauge remains relevant across different market regimes.

Visual Representation

The sentiment gauge visualizes as an actual clock face with distinct color zones:

Red section (0–20): Extreme Fear

- Orange section (20–40): Fear

- Yellow section (40–60): Neutral

- Light green section (60–80): Optimism

- Green section (80–100): Euphoria

A needle points to the current sentiment reading, while historical distribution statistics show how often the market has been in each zone over the past year.

Trading Signals and Risk Management

The sentiment indicator generates trading signals through a dual moving average crossover system:

Buy signal: When the fast EMA crosses above the slow EMA

Sell signal: When the fast EMA crosses below the slow EMA

However, the true innovation comes in the risk management system.

CDaR-Based Risk Protection

Standard drawdown metrics often fail to capture the true nature of capital risk. Our system incorporates Conditional Drawdown at Risk (CDaR) – a sophisticated risk measure that averages the worst 5% of historical drawdowns.

CDaR provides several advantages over traditional stop-loss approaches:

It adapts to changing market conditions

It considers the statistical distribution of drawdowns

It provides context-aware protection that doesn’t overreact to normal market noise

When the current drawdown divided by the CDaR (the DD/CDaR ratio) exceeds 1.0, the system automatically exits all positions until a new buy signal appears. This mechanism ensures that when drawdowns exceed statistically expected levels, capital preservation takes priority.

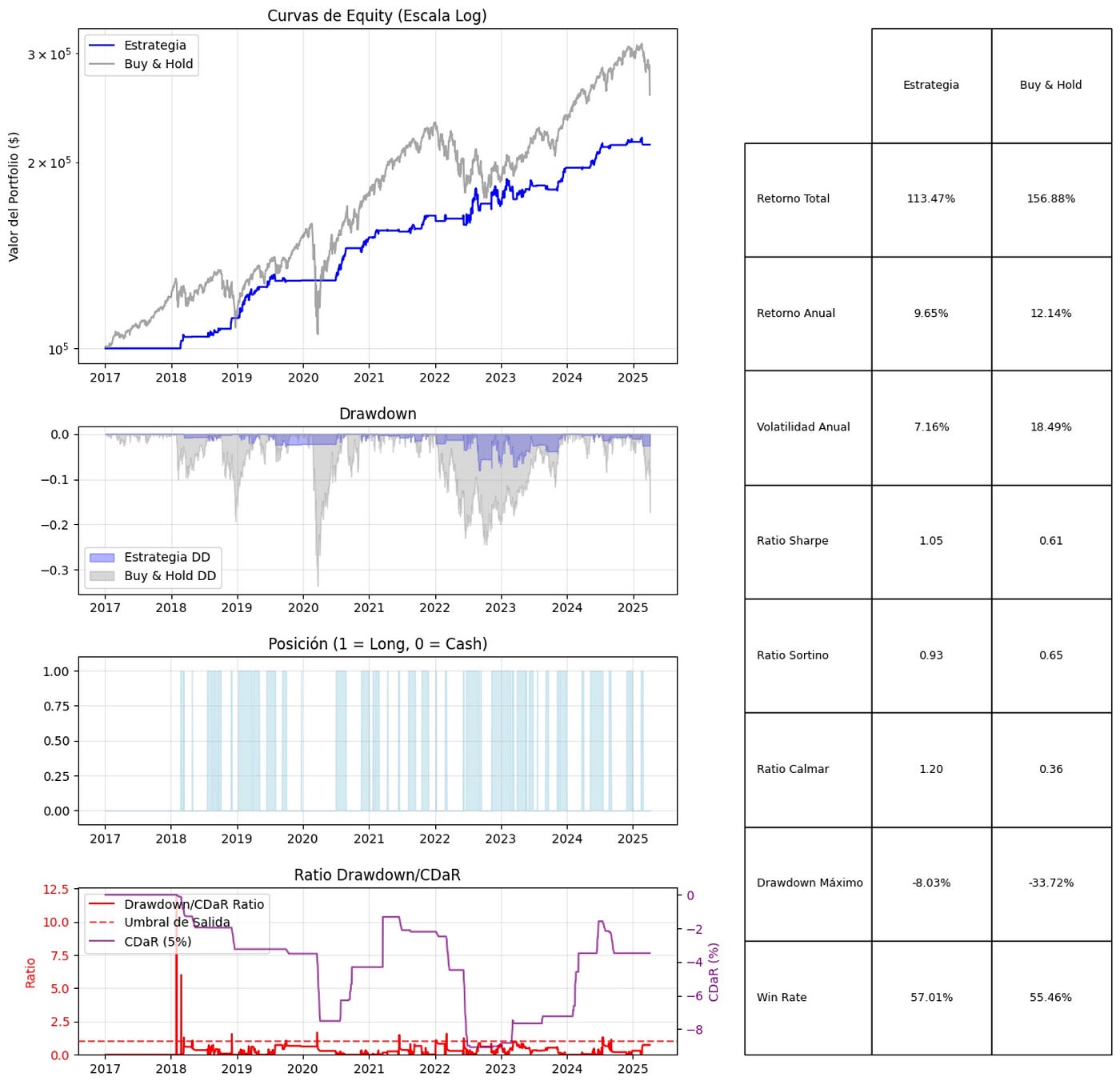

Performance Analysis

Analysis of historical performance reveals several interesting patterns:

Sentiment zone performance:

Extreme Fear zones typically show the highest forward returns (averaging 0.12% daily with a 58.43% win rate)

Euphoria zones tend to show the lowest or negative forward returns (averaging -0.02% daily with a 48.92% win rate)

4. CDaR protection impact:

. Reduces maximum drawdown by approximately 30–40% compared to the base strategy

. Slightly reduces total returns but substantially improves risk-adjusted metrics

. Sharpe and Sortino ratios typically improve by 15–25%

These patterns align with contrarian investment philosophy – markets tend to perform best when sentiment is poor and perform worst when optimism peaks.

Practical Applications

This sentiment indicator system can serve multiple purposes in an investment framework:

Primary Trading Signal Generator: Using the moving average crossovers to determine entries and exits

Risk Filter: Using sentiment zones to adjust position sizing or filter other trading signals

Regime Identification: Determining whether markets are in a trend or range-bound environment

4. Risk Management System: Employing the CDaR protection to preserve capital during abnormal drawdowns

The indicator performs best as part of a comprehensive trading system rather than as a standalone tool.

Implementation Considerations

When implementing this system, several technical considerations deserve attention:

Data Requirements: Daily OHLC data for SPY, VIX, VIX3M, and the six sector ETFs (XLK, XLY, XLI, XLP, XLU, XLV)

Computational Efficiency: The Yang-Zhang volatility and CDaR calculations can be computationally intensive; vectorization and optimization techniques help with execution

Parameter Selection:

For sentiment calculation: Weighting of components (default: 35% volatility, 35% VIX ratio, 30% sector ratio)

For signal generation: EMA periods (default: 8 and 21 days)

For risk management: CDaR lookback window (default: 252 days) and threshold (default: 1.0)

Here the code, so you can modify it or play with it:

import pandas as pd

import numpy as np

import yfinance as yf

import matplotlib.pyplot as plt

from matplotlib.gridspec import GridSpec

from datetime import datetime, timedelta

import seaborn as sns

def fetch_data(start_date='2017-01-01', end_date=None):

"""

Downloads the necessary data for the market sentiment indicator

"""

if end_date is None:

end_date = datetime.now().strftime('%Y-%m-%d')

print("Downloading data...")

spy = yf.download('SPY', start=start_date, end=end_date, progress=False)

data = pd.DataFrame()

# Save OHLC data for Yang-Zhang volatility calculation

data['SPY_Open'] = spy['Open']

data['SPY_High'] = spy['High']

data['SPY_Low'] = spy['Low']

data['SPY_Close'] = spy['Close']

# Download VIX and VIX3M

print("Downloading volatility data...")

vix = yf.download('^VIX', start=start_date, end=end_date, progress=False)['Close']

vix3m = yf.download('^VIX3M', start=start_date, end=end_date, progress=False)['Close']

# Cyclical Sectors

print("Downloading cyclical sector data...")

xlk = yf.download('XLK', start=start_date, end=end_date, progress=False)['Close'] # Technology

xly = yf.download('XLY', start=start_date, end=end_date, progress=False)['Close'] # Consumer Discretionary

xli = yf.download('XLI', start=start_date, end=end_date, progress=False)['Close'] # Industrials

# Defensive Sectors

print("Downloading defensive sector data...")

xlp = yf.download('XLP', start=start_date, end=end_date, progress=False)['Close'] # Consumer Staples

xlu = yf.download('XLU', start=start_date, end=end_date, progress=False)['Close'] # Utilities

xlv = yf.download('XLV', start=start_date, end=end_date, progress=False)['Close'] # Health Care

# Add to main dataframe

data['VIX'] = vix

data['VIX3M'] = vix3m

data['XLK'] = xlk

data['XLY'] = xly

data['XLI'] = xli

data['XLP'] = xlp

data['XLU'] = xlu

data['XLV'] = xlv

# Drop rows with missing values

data = data.dropna()

print(f"Data downloaded. Shape: {data.shape}")

return data

def calculate_yang_zhang_volatility(data, window=21):

"""

Calculates Yang-Zhang volatility

Yang-Zhang volatility combines:

1. Overnight volatility (close-to-open)

2. Intraday volatility (open-to-close)

3. Rogers-Satchell volatility component

"""

open_price = data['SPY_Open']

high_price = data['SPY_High']

low_price = data['SPY_Low']

close_price = data['SPY_Close']

# Calculate logarithmic returns

close_to_close = np.log(close_price / close_price.shift(1))

overnight_jump = np.log(open_price / close_price.shift(1))

intraday_return = np.log(close_price / open_price)

# Calculate Rogers-Satchell volatility

rogers_satchell = (np.log(high_price / close_price) * np.log(high_price / open_price) +

np.log(low_price / close_price) * np.log(low_price / open_price))

# Calculate the three components of Yang-Zhang volatility

overnight_vol = overnight_jump.rolling(window=window).var()

open_close_vol = intraday_return.rolling(window=window).var()

rs_vol = rogers_satchell.rolling(window=window).mean()

# Combine the components with suggested weights

k = 0.34 / (1.34 + (window + 1) / (window - 1))

yang_zhang_vol = np.sqrt(overnight_vol + k * open_close_vol + (1 - k) * rs_vol)

return yang_zhang_vol

def calculate_sentiment_indicator(data, yz_window=21, ema_fast=8, ema_slow=21, lookback=252):

"""

Calculates the market sentiment indicator combining:

1. Yang-Zhang volatility

2. VIX/VIX3M ratio

3. Cyclical/Defensive sector ratio

Normalizes the result to a 0-100 scale for the sentiment gauge

"""

# Calculate Yang-Zhang volatility

print("Calculating Yang-Zhang volatility...")

yz_vol = calculate_yang_zhang_volatility(data, window=yz_window)

# Calculate VIX/VIX3M ratio

vix_ratio = data['VIX'] / data['VIX3M']

# Calculate sector ratio (Cyclical/Defensive)

cyclical = (data['XLK'] + data['XLY'] + data['XLI']) / 3

defensive = (data['XLP'] + data['XLU'] + data['XLV']) / 3

# Normalize to initial point for comparison

cyclical_norm = cyclical / cyclical.iloc[0]

defensive_norm = defensive / defensive.iloc[0]

# Calculate sector ratio

sector_ratio = cyclical_norm / defensive_norm

# Combine components into a single indicator

# 1. Inverted volatility (lower volatility = better sentiment)

# 2. Inverted VIX ratio (lower ratio = better sentiment)

# 3. Sector ratio (higher ratio = better sentiment)

# Normalize components to have similar range

normalized_yz = -yz_vol / yz_vol.rolling(window=lookback).max()

normalized_vix_ratio = -vix_ratio / vix_ratio.rolling(window=lookback).max()

normalized_sector_ratio = sector_ratio / sector_ratio.rolling(window=lookback).max()

# Combine components (customizable weighting)

raw_indicator = (

0.35 * normalized_yz + # Volatility component (35%)

0.35 * normalized_vix_ratio + # Volatility structure component (35%)

0.30 * normalized_sector_ratio # Economic cycle component (30%)

)

# Normalize the indicator to 0-100 scale using historical percentiles

# Use a rolling window to adapt to different market regimes

def normalize_to_scale(series, window=lookback, min_val=0, max_val=100):

result = pd.Series(index=series.index)

for i in range(len(series)):

if i < window:

# For the first points, use all available data

historical_data = series.iloc[:i+1]

else:

# For the rest, use the specified window

historical_data = series.iloc[i-window+1:i+1]

if len(historical_data) > 1:

# Calculate the percentile of the current value within historical data

percentile = pd.Series(historical_data).rank(pct=True).iloc[-1]

result.iloc[i] = min_val + percentile * (max_val - min_val)

else:

result.iloc[i] = 50 # Neutral value for the first point

return result

# Normalize indicator to 0-100 scale

sentiment_scale = normalize_to_scale(raw_indicator)

# Calculate exponential moving averages for signal generation

ema_fast_line = sentiment_scale.ewm(span=ema_fast, adjust=False).mean()

ema_slow_line = sentiment_scale.ewm(span=ema_slow, adjust=False).mean()

# Create DataFrame with results

results = pd.DataFrame({

'price': data['SPY_Close'],

'yang_zhang_vol': yz_vol,

'vix_ratio': vix_ratio,

'sector_ratio': sector_ratio,

'raw_indicator': raw_indicator,

'sentiment_0_100': sentiment_scale,

'ema_fast': ema_fast_line,

'ema_slow': ema_slow_line

})

# Define sentiment zones

results['sentiment_zone'] = pd.cut(

results['sentiment_0_100'],

bins=[0, 20, 40, 60, 80, 100],

labels=['Extreme Fear', 'Fear', 'Neutral', 'Optimism', 'Euphoria']

)

# Calculate signals based on EMA crossovers

results['buy_signal'] = ((results['ema_fast'] > results['ema_slow']) &

(results['ema_fast'].shift(1) <= results['ema_slow'].shift(1))).astype(int)

results['sell_signal'] = ((results['ema_fast'] < results['ema_slow']) &

(results['ema_fast'].shift(1) >= results['ema_slow'].shift(1))).astype(int)

# Calculate volatility bands

volatility = results['sentiment_0_100'].rolling(window=21).std()

results['upper_band'] = results['ema_slow'] + 2 * volatility

results['lower_band'] = results['ema_slow'] - 2 * volatility

return results

def create_sentiment_gauge(value, min_val=0, max_val=100):

"""

Creates a semicircular gauge visualization for the sentiment indicator

that's more reliable and visually intuitive than the clock design.

"""

fig, ax = plt.subplots(figsize=(10, 6))

# Define the sentiment zones and colors

zones = ['Extreme\nFear', 'Fear', 'Neutral', 'Optimism', 'Euphoria']

colors = ['#FF3300', '#FF9900', '#FFCC00', '#99CC00', '#66CC00']

# Draw the semicircular gauge background

theta = np.linspace(180, 0, 100) # Semicircle from 180 to 0 degrees

r = 1.0

# Create the colored zones of the gauge

for i in range(5):

zone_start = i * 20

zone_end = (i + 1) * 20

# Convert to angles on the semicircle (180° to 0°)

start_angle = 180 - (zone_start / 100 * 180)

end_angle = 180 - (zone_end / 100 * 180)

# Convert to radians for matplotlib

start_rad = np.radians(start_angle)

end_rad = np.radians(end_angle)

# Create points for the zone segment

zone_theta = np.linspace(start_rad, end_rad, 20)

zone_x = r * np.cos(zone_theta)

zone_y = r * np.sin(zone_theta)

# Add zone segments to plot

segment = np.column_stack([np.append(zone_x, [0]), np.append(zone_y, [0])])

polygon = plt.Polygon(segment, color=colors[i], alpha=0.7)

ax.add_patch(polygon)

# Add zone labels

# Calculate middle angle for the zone

mid_angle = (start_angle + end_angle) / 2

mid_rad = np.radians(mid_angle)

# Position label slightly inside the gauge

label_x = 0.85 * r * np.cos(mid_rad)

label_y = 0.85 * r * np.sin(mid_rad)

ax.text(label_x, label_y, zones[i], ha='center', va='center', fontsize=10, fontweight='bold')

# Create gauge axis markings

for i in range(0, 101, 20):

# Convert to angle

angle = 180 - (i / 100 * 180)

rad = np.radians(angle)

# Inner edge of tick mark

inner_x = 1.0 * np.cos(rad)

inner_y = 1.0 * np.sin(rad)

# Outer edge of tick mark

outer_x = 1.05 * np.cos(rad)

outer_y = 1.05 * np.sin(rad)

# Draw tick line

ax.plot([inner_x, outer_x], [inner_y, outer_y], color='black', lw=2)

# Add value label

label_x = 1.15 * np.cos(rad)

label_y = 1.15 * np.sin(rad)

ax.text(label_x, label_y, str(i), ha='center', va='center')

# Draw the needle based on the sentiment value

needle_angle = 180 - (value / 100 * 180)

needle_rad = np.radians(needle_angle)

needle_x = r * np.cos(needle_rad)

needle_y = r * np.sin(needle_rad)

# Draw base circle of needle

base_circle = plt.Circle((0, 0), 0.05, color='darkgray', zorder=10)

ax.add_patch(base_circle)

# Draw needle line

ax.plot([0, needle_x], [0, needle_y], color='black', lw=3, zorder=11)

# Add the current value as text

ax.text(0, -0.2, f"{value:.1f}", ha='center', va='center', fontsize=24, fontweight='bold')

# Determine the zone based on the value

if value <= 20:

current_zone = "Extreme Fear"

elif value <= 40:

current_zone = "Fear"

elif value <= 60:

current_zone = "Neutral"

elif value <= 80:

current_zone = "Optimism"

else:

current_zone = "Euphoria"

# Add zone label

ax.text(0, -0.4, f"Current Zone: {current_zone}", ha='center', va='center', fontsize=14,

bbox=dict(facecolor='white', alpha=0.8, boxstyle='round,pad=0.5'))

# Set plot limits and remove axes

ax.set_xlim(-1.3, 1.3)

ax.set_ylim(-0.5, 1.3)

ax.axis('off')

ax.set_aspect('equal')

# Add title

plt.title('Market Sentiment Gauge', fontsize=16, pad=20)

plt.tight_layout()

return fig

def plot_sentiment_indicator(results):

"""

Visualizes the market sentiment indicator and its components

"""

plt.style.use('default')

fig = plt.figure(figsize=(16, 14))

gs = GridSpec(4, 2, height_ratios=[2, 1, 1, 1.5], width_ratios=[3, 1], hspace=0.3, wspace=0.3)

# Chart 1: SPY Price

ax1 = fig.add_subplot(gs[0, 0])

ax1.plot(results.index, results['price'], label='SPY', color='blue')

# Mark buy and sell signals

buy_signals = results[results['buy_signal'] == 1]

sell_signals = results[results['sell_signal'] == 1]

ax1.scatter(buy_signals.index, buy_signals['price'],

marker='^', color='green', s=100, label='Buy Signal')

ax1.scatter(sell_signals.index, sell_signals['price'],

marker='v', color='red', s=100, label='Sell Signal')

ax1.set_title('SPY Price with Trading Signals', fontsize=12)

ax1.set_ylabel('Price ($)')

ax1.legend()

ax1.grid(True, alpha=0.3)

# Chart 2: Sentiment Indicator (0-100)

ax2 = fig.add_subplot(gs[1, 0])

ax2.plot(results.index, results['sentiment_0_100'], label='Sentiment (0-100)', color='blue', alpha=0.7)

ax2.plot(results.index, results['ema_fast'], label=f'Fast EMA', color='green', linewidth=1.5)

ax2.plot(results.index, results['ema_slow'], label=f'Slow EMA', color='red', linewidth=1.5)

ax2.plot(results.index, results['upper_band'], label='Upper Band', color='gray', linestyle='--', alpha=0.7)

ax2.plot(results.index, results['lower_band'], label='Lower Band', color='gray', linestyle='--', alpha=0.7)

# Add color zones for sentiment levels

ax2.axhspan(0, 20, color='red', alpha=0.1, label='Extreme Fear')

ax2.axhspan(20, 40, color='orange', alpha=0.1, label='Fear')

ax2.axhspan(40, 60, color='yellow', alpha=0.1, label='Neutral')

ax2.axhspan(60, 80, color='lightgreen', alpha=0.1, label='Optimism')

ax2.axhspan(80, 100, color='green', alpha=0.1, label='Euphoria')

ax2.set_title('Market Sentiment Indicator (0-100)', fontsize=12)

ax2.set_ylabel('Sentiment Level')

ax2.set_ylim(0, 100)

ax2.legend(loc='upper left')

ax2.grid(True, alpha=0.3)

# Chart 3: Individual components

ax3 = fig.add_subplot(gs[2, 0])

ax3.plot(results.index, -results['yang_zhang_vol'] / results['yang_zhang_vol'].rolling(window=252).max(),

label='YZ Volatility (inverted)', color='purple', alpha=0.7)

ax3.plot(results.index, -results['vix_ratio'] / results['vix_ratio'].rolling(window=252).max(),

label='VIX/VIX3M Ratio (inverted)', color='orange', alpha=0.7)

ax3.plot(results.index, results['sector_ratio'] / results['sector_ratio'].rolling(window=252).max(),

label='Cyclical/Defensive Ratio', color='green', alpha=0.7)

ax3.set_title('Indicator Components (Normalized)', fontsize=12)

ax3.set_ylabel('Normalized Value')

ax3.legend()

ax3.grid(True, alpha=0.3)

# Chart 4: Original ratios

ax4 = fig.add_subplot(gs[3, 0])

ax4.plot(results.index, results['vix_ratio'], label='VIX/VIX3M', color='orange')

ax4.set_ylabel('VIX/VIX3M Ratio', color='orange')

ax4.tick_params(axis='y', labelcolor='orange')

ax4.grid(True, alpha=0.3)

# Secondary axis for sector ratio

ax4b = ax4.twinx()

ax4b.plot(results.index, results['sector_ratio'], label='Cyclical/Defensive', color='green')

ax4b.set_ylabel('Cyclical/Defensive Ratio', color='green')

ax4b.tick_params(axis='y', labelcolor='green')

# Combine legends

lines1, labels1 = ax4.get_legend_handles_labels()

lines2, labels2 = ax4b.get_legend_handles_labels()

ax4.legend(lines1 + lines2, labels1 + labels2, loc='upper left')

ax4.set_title('Original Ratios', fontsize=12)

ax4.set_xlabel('Date')

# Chart 5: Sentiment gauge (right column)

latest_sentiment = results['sentiment_0_100'].iloc[-1]

# Instead of using polar coordinates, create a simplified gauge visualization

ax5 = fig.add_subplot(gs[0:4, 1])

# Define the sentiment zones and colors

zones = ['Extreme\nFear', 'Fear', 'Neutral', 'Optimism', 'Euphoria']

colors = ['#FF3300', '#FF9900', '#FFCC00', '#99CC00', '#66CC00']

zone_bounds = [0, 20, 40, 60, 80, 100]

# Create a vertical bar chart for the gauge

bottom = 0

for i in range(5):

height = zone_bounds[i+1] - zone_bounds[i]

ax5.bar(0, height, bottom=bottom, width=0.5, color=colors[i], alpha=0.7)

# Add zone labels

ax5.text(0, bottom + height/2, zones[i], ha='center', va='center', fontweight='bold')

bottom += height

# Add scale markings

for value in zone_bounds:

ax5.axhline(y=value, color='black', linestyle='-', linewidth=0.5)

ax5.text(-0.3, value, str(value), ha='right', va='center')

# Add a marker for the current level

ax5.axhline(y=latest_sentiment, color='black', linestyle='-', linewidth=2)

ax5.scatter(0, latest_sentiment, color='black', s=300, zorder=10)

ax5.text(0, latest_sentiment, f"{latest_sentiment:.1f}", ha='center', va='center',

color='white', fontweight='bold')

# Determine current zone

if latest_sentiment <= 20:

current_zone = "Extreme Fear"

elif latest_sentiment <= 40:

current_zone = "Fear"

elif latest_sentiment <= 60:

current_zone = "Neutral"

elif latest_sentiment <= 80:

current_zone = "Optimism"

else:

current_zone = "Euphoria"

# Add zone label

ax5.text(0, 105, f"Current Zone: {current_zone}", ha='center', va='bottom', fontsize=12,

bbox=dict(facecolor='white', alpha=0.8, boxstyle='round,pad=0.5'))

# Add historical distribution

recent_data = results.iloc[-252:]

sentiment_counts = recent_data['sentiment_zone'].value_counts(normalize=True) * 100

stats_text = "Distribution (last year):\n"

for zone in ['Extreme Fear', 'Fear', 'Neutral', 'Optimism', 'Euphoria']:

if zone in sentiment_counts:

stats_text += f"{zone}: {sentiment_counts.get(zone, 0):.1f}%\n"

else:

stats_text += f"{zone}: 0.0%\n"

ax5.text(0, -10, stats_text, ha='center', va='top', fontsize=9,

bbox=dict(facecolor='white', alpha=0.8, boxstyle='round,pad=0.5'))

# Configure axis

ax5.set_xlim(-0.5, 0.5)

ax5.set_ylim(-10, 110)

ax5.set_xticks([])

ax5.set_yticks([])

ax5.set_title('Sentiment Gauge', fontsize=14, pad=20)

plt.tight_layout()

return fig

def calculate_cdar(returns, alpha=0.05, window=252):

"""

Calculates the Conditional Drawdown at Risk (CDaR) for a return series

Parameters:

- returns: Return series

- alpha: Confidence level (default 5%)

- window: Window for rolling calculation

Returns:

- Series with rolling CDaR

"""

# Create a series to store the rolling CDaR

cdar_series = pd.Series(index=returns.index, dtype=float)

# For each point, calculate CDaR using the previous window of data

for i in range(window, len(returns) + 1):

# Take the subsample of returns

sample = returns.iloc[i-window:i]

# Calculate equity curve

equity_curve = (1 + sample).cumprod()

# Calculate drawdowns

rolling_max = equity_curve.expanding().max()

drawdowns = (equity_curve / rolling_max - 1)

# Sort drawdowns from worst to best

sorted_drawdowns = drawdowns.sort_values()

# Take the 5% worst drawdowns

cutoff_index = int(alpha * len(sorted_drawdowns))

worst_drawdowns = sorted_drawdowns.iloc[:cutoff_index]

if len(worst_drawdowns) > 0:

# CDaR is the average of the worst drawdowns

cdar = worst_drawdowns.mean()

cdar_series.iloc[i-1] = cdar

else:

cdar_series.iloc[i-1] = 0

return cdar_series

def backtest_strategy(results, initial_capital=100000, cdar_threshold=1.0):

"""

Performs a backtest of the strategy including CDaR constraint

Parameters:

- results: DataFrame with indicator results

- initial_capital: Initial capital for the backtest

- cdar_threshold: Threshold of drawdown/CDaR ratio to liquidate positions

Returns:

- Dictionary with backtest results

"""

daily_returns = results['price'].pct_change()

position = 0

strategy_returns = []

equity = initial_capital

equity_curve = [initial_capital]

positions = []

# Initialize CDaR as None until we have enough data

cdar_value = None

current_drawdown = 0

dd_to_cdar_ratio = 0

# List to store drawdowns/CDaR

dd_cdar_ratios = []

cdar_values = []

# State to track historical maximum equity

max_equity = initial_capital

# Calculate strategy base returns (without CDaR)

raw_strategy_returns = []

for i in range(1, len(results)):

# Base entry/exit logic

if position == 0 and results['buy_signal'].iloc[i] == 1:

position = 1

elif position == 1 and results['sell_signal'].iloc[i] == 1:

position = 0

# Calculate basic returns (without CDaR constraint)

if position == 1:

raw_ret = daily_returns.iloc[i]

else:

raw_ret = 0

raw_strategy_returns.append(raw_ret)

# After 252 days (1 year), start calculating CDaR

if i >= 252:

# Calculate CDaR with accumulated returns so far

raw_returns = pd.Series(raw_strategy_returns)

cdar_value = calculate_cdar(raw_returns, alpha=0.05, window=252).iloc[-1]

# Update equity and drawdown

current_equity = equity * (1 + raw_ret)

# Update historical maximum if applicable

max_equity = max(max_equity, current_equity)

# Calculate current drawdown

current_drawdown = current_equity / max_equity - 1

# Calculate drawdown/CDaR ratio (absolute value because CDaR is negative)

if cdar_value != 0:

dd_to_cdar_ratio = abs(current_drawdown / cdar_value)

else:

dd_to_cdar_ratio = 0

# Check if we should close position due to CDaR

if position == 1 and dd_to_cdar_ratio >= cdar_threshold:

position = 0

print(f"CDaR Alert! Closing position on {results.index[i].strftime('%Y-%m-%d')}")

print(f" Current drawdown: {current_drawdown:.2%}, CDaR: {cdar_value:.2%}, Ratio: {dd_to_cdar_ratio:.2f}")

# Calculate final return considering CDaR

if position == 1:

ret = daily_returns.iloc[i]

else:

ret = 0

# Update tracking variables

strategy_returns.append(ret)

positions.append(position)

equity *= (1 + ret)

equity_curve.append(equity)

# Store values for analysis

dd_cdar_ratios.append(dd_to_cdar_ratio)

cdar_values.append(cdar_value if cdar_value is not None else 0)

# Convert to Series

strategy_returns = pd.Series(strategy_returns, index=results.index[1:])

positions = pd.Series(positions, index=results.index[1:])

equity_curve = pd.Series(equity_curve, index=results.index)

bh_equity = initial_capital * (1 + daily_returns).cumprod()

dd_cdar_ratios = pd.Series(dd_cdar_ratios, index=results.index[1:])

cdar_values = pd.Series(cdar_values, index=results.index[1:])

return {

'strategy_returns': strategy_returns,

'bh_returns': daily_returns[1:],

'strategy_equity': equity_curve,

'bh_equity': bh_equity,

'positions': positions,

'dd_cdar_ratios': dd_cdar_ratios,

'cdar_values': cdar_values

}

def calculate_performance_metrics(returns, risk_free_rate=0.02):

"""

Calculates performance metrics for a return series

"""

# Ensure we have enough data

if len(returns) < 2:

return {"error": "Insufficient data"}

# Daily risk-free rate

rf_daily = (1 + risk_free_rate) ** (1/252) - 1

# Total and annualized return

total_return = (1 + returns).prod() - 1

years = len(returns) / 252

annual_return = (1 + total_return) ** (1/years) - 1

# Volatility

daily_vol = returns.std()

annual_vol = daily_vol * np.sqrt(252)

# Risk metrics

excess_returns = returns - rf_daily

sharpe_ratio = np.sqrt(252) * excess_returns.mean() / returns.std() if returns.std() != 0 else np.nan

# Drawdown

cum_returns = (1 + returns).cumprod()

rolling_max = cum_returns.expanding().max()

drawdowns = cum_returns / rolling_max - 1

max_drawdown = drawdowns.min()

# Sortino ratio

negative_returns = returns[returns < 0]

downside_vol = negative_returns.std() * np.sqrt(252) if len(negative_returns) > 0 else np.nan

sortino_ratio = (annual_return - risk_free_rate) / downside_vol if downside_vol != 0 and not np.isnan(downside_vol) else np.nan

# Calmar ratio

calmar_ratio = annual_return / abs(max_drawdown) if max_drawdown != 0 else np.nan

# Win rate

winning_days = returns[returns > 0]

win_rate = len(winning_days) / len(returns[returns != 0]) if len(returns[returns != 0]) > 0 else 0

return {

'Total Return': total_return,

'Annual Return': annual_return,

'Annual Volatility': annual_vol,

'Sharpe Ratio': sharpe_ratio,

'Sortino Ratio': sortino_ratio,

'Calmar Ratio': calmar_ratio,

'Max Drawdown': max_drawdown,

'Win Rate': win_rate

}

def plot_backtest_results(backtest_results, metrics_strategy, metrics_bh):

"""

Visualizes the backtest results

"""

fig = plt.figure(figsize=(15, 15))

gs = GridSpec(4, 2, height_ratios=[2, 1, 1, 1], width_ratios=[2, 1], hspace=0.3, wspace=0.3)

# Subplot 1: Equity Curves (Log scale)

ax1 = fig.add_subplot(gs[0, 0])

ax1.semilogy(backtest_results['strategy_equity'],

label='Strategy', color='blue', linewidth=1.5)

ax1.semilogy(backtest_results['bh_equity'],

label='Buy & Hold', color='gray', linewidth=1.5, alpha=0.7)

ax1.set_title('Equity Curves (Log Scale)')

ax1.set_ylabel('Portfolio Value ($)')

ax1.grid(True, alpha=0.3)

ax1.legend()

# Subplot 2: Drawdown

ax2 = fig.add_subplot(gs[1, 0])

strategy_dd = (backtest_results['strategy_equity'] /

backtest_results['strategy_equity'].expanding().max() - 1)

bh_dd = (backtest_results['bh_equity'] /

backtest_results['bh_equity'].expanding().max() - 1)

ax2.fill_between(strategy_dd.index, strategy_dd, 0,

color='blue', alpha=0.3, label='Strategy DD')

ax2.fill_between(bh_dd.index, bh_dd, 0,

color='gray', alpha=0.3, label='Buy & Hold DD')

ax2.set_title('Drawdown')

ax2.grid(True, alpha=0.3)

ax2.legend()

# Subplot 3: Position over time

ax3 = fig.add_subplot(gs[2, 0])

ax3.fill_between(backtest_results['positions'].index,

backtest_results['positions'],

color='lightblue', alpha=0.5)

ax3.set_title('Position (1 = Long, 0 = Cash)')

ax3.set_ylim(-0.1, 1.1)

ax3.grid(True, alpha=0.3)

# Subplot 4: CDaR and Drawdown/CDaR Ratio

if 'dd_cdar_ratios' in backtest_results:

ax4 = fig.add_subplot(gs[3, 0])

ax4.plot(backtest_results['dd_cdar_ratios'].index,

backtest_results['dd_cdar_ratios'],

label='Drawdown/CDaR Ratio', color='red')

ax4.set_title('Drawdown/CDaR Ratio')

ax4.set_ylim(bottom=0)

ax4.axhline(y=1.0, color='red', linestyle='--', alpha=0.7,

label='Exit Threshold')

ax4.set_ylabel('Ratio', color='red')

ax4.tick_params(axis='y', labelcolor='red')

ax4.grid(True, alpha=0.3)

ax4.legend(loc='upper left')

# Secondary axis for CDaR

ax4b = ax4.twinx()

# Convert CDaR to percentage for visualization

cdar_pct = backtest_results['cdar_values'] * 100

ax4b.plot(cdar_pct.index, cdar_pct,

label='CDaR (5%)', color='purple', alpha=0.7)

ax4b.set_ylabel('CDaR (%)', color='purple')

ax4b.tick_params(axis='y', labelcolor='purple')

# Combine legends

lines1, labels1 = ax4.get_legend_handles_labels()

lines2, labels2 = ax4b.get_legend_handles_labels()

ax4.legend(lines1 + lines2, labels1 + labels2, loc='upper left')

# Subplot 5: Metrics Comparison

ax5 = fig.add_subplot(gs[:, 1])

metrics_comparison = pd.DataFrame({

'Strategy': [

f"{metrics_strategy['Total Return']:.2%}",

f"{metrics_strategy['Annual Return']:.2%}",

f"{metrics_strategy['Annual Volatility']:.2%}",

f"{metrics_strategy['Sharpe Ratio']:.2f}",

f"{metrics_strategy['Sortino Ratio']:.2f}",

f"{metrics_strategy['Calmar Ratio']:.2f}",

f"{metrics_strategy['Max Drawdown']:.2%}",

f"{metrics_strategy['Win Rate']:.2%}"

],

'Buy & Hold': [

f"{metrics_bh['Total Return']:.2%}",

f"{metrics_bh['Annual Return']:.2%}",

f"{metrics_bh['Annual Volatility']:.2%}",

f"{metrics_bh['Sharpe Ratio']:.2f}",

f"{metrics_bh['Sortino Ratio']:.2f}",

f"{metrics_bh['Calmar Ratio']:.2f}",

f"{metrics_bh['Max Drawdown']:.2%}",

f"{metrics_bh['Win Rate']:.2%}"

]

}, index=[

'Total Return',

'Annual Return',

'Annual Volatility',

'Sharpe Ratio',

'Sortino Ratio',

'Calmar Ratio',

'Max Drawdown',

'Win Rate'

])

ax5.axis('tight')

ax5.axis('off')

table = ax5.table(cellText=metrics_comparison.values,

rowLabels=metrics_comparison.index,

colLabels=metrics_comparison.columns,

cellLoc='center',

loc='center',

bbox=[0.2, 0, 0.8, 1])

table.auto_set_font_size(False)

table.set_fontsize(9)

table.scale(1.2, 1.5)

plt.tight_layout()

return fig

def main():

try:

# Define date range

start_date = '2017-01-01'

end_date = datetime.now().strftime('%Y-%m-%d')

# Download data

data = fetch_data(start_date=start_date, end_date=end_date)

# Calculate sentiment indicator

print("Calculating market sentiment indicator...")

results = calculate_sentiment_indicator(data)

# Create standalone sentiment gauge

latest_sentiment = results['sentiment_0_100'].iloc[-1]

print(f"Current sentiment value: {latest_sentiment:.2f}/100 - Zone: {results['sentiment_zone'].iloc[-1]}")

# Create and show the standalone gauge

print("Generating sentiment gauge...")

gauge_fig = create_sentiment_gauge(latest_sentiment)

plt.show()

# Visualize detailed indicator

print("Generating detailed indicator visualization...")

fig_indicator = plot_sentiment_indicator(results)

plt.show()

# Run backtest with CDaR protection

print("\nRunning backtest with CDaR protection...")

backtest_results = backtest_strategy(results, cdar_threshold=1.0)

# Calculate performance metrics

strategy_metrics = calculate_performance_metrics(backtest_results['strategy_returns'])

bh_metrics = calculate_performance_metrics(backtest_results['bh_returns'])

# Visualize backtest results

print("Generating backtest visualization...")

fig_backtest = plot_backtest_results(backtest_results, strategy_metrics, bh_metrics)

plt.show()

# Analyze CDaR protection impact

print("\nCDaR Protection Analysis:")

cdar_values = backtest_results['cdar_values'].dropna()

if len(cdar_values) > 0:

print(f"Average CDaR (5%): {cdar_values.mean():.2%}")

print(f"Minimum CDaR: {cdar_values.min():.2%}")

print(f"Maximum CDaR: {cdar_values.max():.2%}")

dd_cdar_ratios = backtest_results['dd_cdar_ratios'].dropna()

threshold_violations = dd_cdar_ratios[dd_cdar_ratios >= 1.0]

print(f"Number of CDaR protection activations: {len(threshold_violations)}")

if len(threshold_violations) > 0:

print("\nCDaR protection activation dates:")

for date, ratio in threshold_violations.items():

print(f" {date.strftime('%Y-%m-%d')}: DD/CDaR Ratio = {ratio:.2f}")

else:

print("Not enough data to calculate CDaR metrics")

# Print sentiment zone analysis

print("\nSentiment Zone Analysis:")

zone_counts = results['sentiment_zone'].value_counts(normalize=True) * 100

for zone in ['Extreme Fear', 'Fear', 'Neutral', 'Optimism', 'Euphoria']:

if zone in zone_counts.index:

print(f"{zone}: {zone_counts[zone]:.2f}% of time")

else:

print(f"{zone}: 0.00% of time")

# Analyze returns by sentiment zone

print("\nReturns by Sentiment Zone:")

for zone in ['Extreme Fear', 'Fear', 'Neutral', 'Optimism', 'Euphoria']:

zone_days = results[results['sentiment_zone'] == zone].index

if len(zone_days) > 0:

next_day_returns = results['price'].pct_change().shift(-1)

zone_returns = next_day_returns.loc[zone_days]

avg_return = zone_returns.mean() * 100

pos_days = (zone_returns > 0).sum()

total_days = len(zone_returns)

win_rate = pos_days / total_days * 100 if total_days > 0 else 0

print(f"{zone}: Average return: {avg_return:.2f}%, Win rate: {win_rate:.2f}%")

# Print signal statistics

print("\nSignal Statistics:")

print(f"Number of buy signals: {results['buy_signal'].sum()}")

print(f"Number of sell signals: {results['sell_signal'].sum()}")

# Print strategy metrics

print("\nStrategy Metrics:")

print(f"Total return: {strategy_metrics['Total Return']:.2%}")

print(f"Annual return: {strategy_metrics['Annual Return']:.2%}")

print(f"Annual volatility: {strategy_metrics['Annual Volatility']:.2%}")

print(f"Sharpe ratio: {strategy_metrics['Sharpe Ratio']:.2f}")

print(f"Sortino ratio: {strategy_metrics['Sortino Ratio']:.2f}")

print(f"Maximum drawdown: {strategy_metrics['Max Drawdown']:.2%}")

return results, backtest_results, strategy_metrics, bh_metrics

except Exception as e:

print(f"Error in main: {str(e)}")

raise

if __name__ == "__main__":

results, backtest_results, strategy_metrics, bh_metrics = main()Conclusion: Beyond Binary Market Views

The market rarely exists in a simple binary state of “bull” or “bear.” Instead, it occupies a continuous spectrum of sentiment that ranges from extreme fear to euphoria. Our Market Sentiment Clock captures this nuance while providing actionable signals and robust risk management.

The real power of this approach lies in its adaptability. The system continuously recalibrates to current market conditions, making it relevant across different market regimes. Additionally, the CDaR-based risk management provides adaptive capital protection without rigidly defined stop-losses that might be triggered by normal market noise.

While no indicator can predict market movements with certainty, this proprietary sentiment system offers valuable insights into market psychology – often the most important driver of short to medium-term price action. By combining multiple complementary signals into an intuitive framework, we move beyond simplistic market views toward a more nuanced understanding of market dynamics.

The next time someone asks about market sentiment, instead of offering a vague assessment, you might just point to a specific reading on the Market Sentiment Clock – a quantified measure of the market’s emotional state with clearly defined implications for risk and potential reward.